America's Electricity Grids: At a Crossroads

Because electricity demand (load) and supply (generation) must be kept in instantaneous balance, electric systems must always maintain adequate resources.

Listen

The Issue

The United States is experiencing growth in electricity demand not seen for decades, driven mainly by the accelerating development of cloud computing and power-hungry artificial-intelligence data centers, alongside bipartisan efforts to reshore major industries. After more than two decades of near-flat demand, recent forecasts see overall national electricity consumption increasing 15% by 2030-and 30%-40% by 2035. Some regions of the country are expected to experience even steeper increases. This resurgence is fundamentally a positive signal for America's economy and its people. Yet it follows years of policies focused mainly on reducing or managing demand, leaving many regions ill-prepared. The sheer scale of these new loads and the unprecedented speed of their deployment pose significant practical, economic, and regulatory challenges.

The surge in electricity demand raises valid concerns about reliability and affordability. Reliability risks stem from the physical and operational characteristics of U.S. electric grids; affordability concerns arise from the massive infrastructure investments required to meet the new demand-and fears that residential and small-business customers could shoulder those costs, rather than the businesses driving the new demand. Political responses to these challenges range from a White House ceremony during which seven major tech companies signed a pledge to cover the costs of meeting their electricity needs to fast-growing resistance movements pushing state and local authorities to ban the construction of data centers. At its core, meeting growing electricity demand is a significant engineering and regulatory challenge: accommodating rapid growth while ensuring rates are "just and reasonable," as required under long-standing electricity law.

The Reality

Few would dispute that electricity is the lifeblood of contemporary society. Greater consumption of this critical secondary energy source-electricity must be generated from primary forms of energy-signals rising economic productivity and human flourishing. When market-driven, electrifying end-uses previously fueled by combustion can deliver greater convenience and efficiency, among other benefits.

Over more than a century, systems of hundreds of electric utilities gradually evolved into a complex web of generating plants, high-voltage transmission lines, and local distribution centers that delivered affordable, safe, and reliable electricity across the country for generations. But that web has frayed, especially over the past 15 years.

Economic and regulatory costs of doing business in the United States prompted many heavy industries to move offshore, even as electric equipment grew more efficient. A prime example is aluminum smelting in the Pacific Northwest. Where once 10 smelters drew on low-cost hydropower from federal dams on the Columbia River, none operate today.

With few exceptions, the sale and delivery of electricity are regulated at both the federal and state levels. State laws control the types and locations of electric generating plants, while state utility regulators use complex methods to determine costs, allocate them across customer classes, and set rates. Moreover, state policies-such as renewable-energy mandates and zero-emissions goals-have shaped the mix of available generating resources, often without fully accounting for the physical impacts on grid reliability and cost. This has destabilized wholesale electric markets-which are regulated at the federal level, along with interstate transmission-and has led to controversial price spikes, such as a tenfold increase in wholesale capacity market prices administered by PJM Interconnection, LLC. PJM is a Federal Energy Regulatory Commission (FERC)-approved Regional Transmission Organization (RTO) responsible for operating the grid in a 13-state region covering the mid-Atlantic states and the District of Columbia. These higher prices signal the urgent need for dispatchable generating resources that can be called upon to produce electricity whenever required.

At the same time, both state and federal energy and environmental policies have promoted the electrification of end-uses-especially vehicles and space heating-while also emphasizing measures to reduce overall consumption. These measures include efficiency mandates and pricing regimes that discourage electricity use at times when it is most convenient for consumers. Consequently, over the first two decades of this century, U.S. electricity demand grew at an annual average rate of less than 0.6%. This near-flat trajectory has left the grid and supply infrastructure under-optimized and unprepared for today's resurgence.

The Evolution of the Electric System

The structure of the U.S. electric system reflects various economic and legal realities. Commercial generation and electricity delivery began in 1882, when Thomas Edison opened the Pearl Street generating station in New York City-the nation's first central power plant. As demand grew, multiple companies entered the market, often stringing competing poles and wires along the same streets. Recognizing the inefficiency and impracticality of duplication, state legislators and regulators established a system of exclusive service territories. Local utilities received monopoly rights to sell electricity within defined geographic franchise areas. In exchange, they assumed an obligation to serve all customers in that territory on reasonable terms.

Because local utilities operated as monopolies, the rates they charged customers had to be set by public-utility regulators. The goal of this long-standing regulatory framework is to balance the interests of utility investors-who provide the capital essential to build and maintain the system-with the need to keep electricity affordable for customers. This structure, called cost-of-service (COS) regulation, allows utilities to recover their prudent costs (those reasonably necessary to provide service) plus a reasonable return on invested capital. The allowed return is calibrated to compensate investors fairly for the risks involved, enabling the utility to attract the financing needed for reliable service.

As electricity demand grew nationwide, utilities recognized that pooling their resources could improve both reliability and efficiency: If one generator suddenly failed, others in the pool could help meet demand. The first such power pool formed in 1927 to coordinate generation among three utilities in Pennsylvania and New Jersey and was later renamed the aforementioned PJM (after a Maryland utility joined in 1956). Subsequently, other regional power pools developed throughout the country.

From the 1920s through the early 1970s, electricity demand and U.S. GDP grew in tandem, both rising steeply as the country electrified. Shocks to the global and domestic energy systems in the 1970s-particularly the Organization of the Petroleum Exporting Countries (OPEC) oil embargoes of 1973 and 1979, followed by recessions and high inflation-caused electricity demand growth to slow sharply and eventually level off. With load growth stalled, utilities canceled many long-planned major power plants, nearly all of them nuclear units then under construction. The recovery of the costs incurred for those plants presented major questions for COS regulation. In many jurisdictions, utility customers were saddled with billions of dollars in sunk costs for plants that were canceled-whether voluntarily by utilities or deemed imprudent by regulators.

This painful experience continues to inform today's debate over new infrastructure investments and explains widespread fears of a repeat: ratepayers once again bearing heavy costs if anticipated demand growth fails to materialize in the coming years. Although the structure of the electric industry today differs substantially from that of half a century ago, the same moral hazard problems persist. Risks and rewards are still borne by different parties, creating misaligned incentives that regulators must carefully manage.

The experiences of the 1970s prompted regulators and policymakers to rethink the electric industry. In 1978, Congress enacted the National Energy Act-a comprehensive package of legislation aimed at reducing dependence on foreign oil. This included subsidies, paid by electric utility customers, for independently developed small power producers or cogeneration units, and requirements that industrial customers reduce their reliance on oil and natural gas in favor of coal. In the 1980s, state regulators increasingly required utilities to implement energy conservation programs and offer incentives or subsidies to encourage customers to improve efficiency or switch away from electric space and water heating.

By the early 1990s, electric customers-especially large industrial ones-were clamoring for additional changes. Frustrated with high rates, they sought to purchase power directly from competitive suppliers rather than from their local regulated utilities. These pressures sparked a broader movement to restructure the electric industry in many states. As a result, utilities were forced to divest their generating plants, transforming them into local distribution companies focused on delivering electricity to retail customers.

California became a trendsetter for electric-industry restructuring when its Public Utilities Commission issued what became known as the Blue Book in 1994. The California assembly passed restructuring legislation in 1996, as did several other early-adopter states. It introduced retail competition while capping the prices that electric utilities could charge. Because competition and price caps don't mix, the state's market design-particularly the mismatch between volatile wholesale prices and capped retail rates-led to a debacle. Nevertheless, another 17 states enacted restructuring measures to varying degrees, allowing customers some ability to choose their electric supplier.

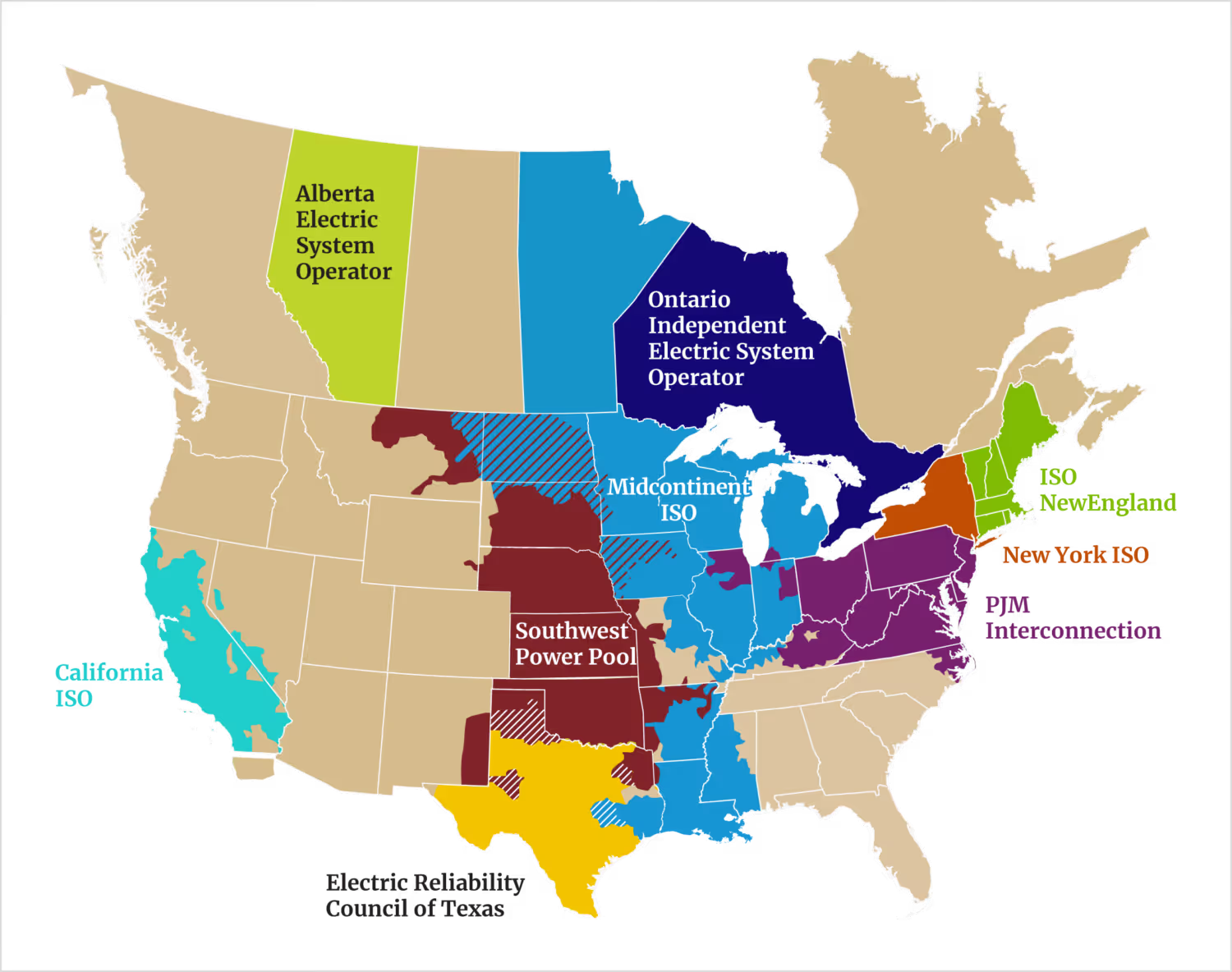

To encourage greater wholesale competition and independently developed generation, the Energy Policy Act of 1992 gave FERC explicit authority to require electric utilities to offer transmission service over their lines to third parties seeking to "wheel" power from distant generators. In 1996, FERC issued Order No. 888, which required open access to high-voltage transmission systems on a nondiscriminatory basis. The order also encouraged wholesale market competition and the formation of Independent System Operators (ISOs), whether by converting existing power pools or building them from the ground up. In 1999, FERC took further action to encourage the formation of RTOs to administer transmission systems and oversee competitive wholesale generation markets (see figure 1). FERC claimed that RTOs would improve competition, reduce costs through greater efficiency, and benefit consumers.

Nevertheless, the Intermountain West, the Pacific Northwest, and the Southeastern U.S. do not have RTOs. Instead, they rely on COS regulation and variants of traditional pooling arrangements. But in the remainder of the country, RTOs have formed and grown in size and complexity. Today, more than two-thirds of electric customers are connected indirectly to an RTO, the largest of which is PJM.

Figure 1. U.S. Regional Transmission Organizations

Empirical studies have found that competitively owned generators tend to operate more efficiently than those owned by vertically integrated utilities, which-under traditional COS regulation-have fewer incentives to improve their operating efficiency. However, simply allowing competition among generators proved insufficient to ensure adequate supply. Additional rules were needed to ensure that enough electricity was available when demand was greatest, typically in the early-morning and early-evening hours.

Because electricity demand (load) and supply (generation) must be kept in instantaneous balance, electric systems must always maintain adequate resources. Historically, state utility regulators required vertically integrated utilities to procure or build sufficient generating capacity to meet projected customer demand. But FERC believed that RTOs could also play a key role in ensuring resource adequacy. Thus, several RTOs (including PJM) developed synthetic capacity markets intended to compensate generation owners for making capacity available when needed. Other RTOs, such as the Electric Reliability Council of Texas (ERCOT), developed entirely different mechanisms.

However, market rules in RTOs have increasingly been influenced by political considerations rather than economic ones. For example, wind and solar facilities can receive discounted payments for the capacity they provide, even though their generation is intermittent and typically does not coincide with peak demand. And demand response customers can be paid to reduce their electricity use when an RTO requests it, but an RTO can do so only a limited number of times each year and for a limited number of hours.

The Situation Today

Perhaps not surprisingly, reliable, dispatchable generating capacity is not being added in RTO regions in the quantities needed to match growing demand. Along with energy markets, capacity markets have not yielded the revenue necessary to support the entry of new generation. Another problem is that the tools available to RTOs are inherently limited. For example, RTOs cannot mandate construction of new generation or directly prevent owners from retiring existing units. Moreover, capacity market rules-along with the requirements for connecting new capacity to the power system-have grown increasingly problematic.

Recent sharp increases in forecast electricity demand have exposed limitations in many current regulatory structures. Dispatchable generating capacity is desperately needed, yet competitive generators and regulated utilities both remain cautious because of substantial financial risks, exemplified by the delays and cost overruns that plagued the expansion of nuclear capacity at Georgia's Plant Vogtle. Similarly, new transmission development has lagged because of onerous siting rules, permitting delays, and high costs. Finally, residential customers and advocacy groups are fighting the development of data centers in many utility territories, claiming that residential and small-business ratepayers will be stuck with the bills because of unsupported claims that existing data centers have been responsible for the observed increases in retail electric rates.

Public and Private Grid Options

Clearly, business-as-usual practices will not suffice. One emerging option that may gain momentum-driven in part by the Ratepayer Protection Pledge and in part by the practical need for speed-is reminiscent of the earliest days of electricity development in the United States: privately developed electric grids with well-defined boundaries that can operate independently or as hybrid solutions in tandem with the broader electric grid. These, too, raise important technical, economic, and legal issues that must be addressed.

In his most recent State of the Union address, President Trump emphasized the "obligation" of "major tech companies . . . to provide for their own power needs." He previewed the Ratepayer Protection Pledge, which was subsequently signed on March 4, 2026, by seven large tech companies: Amazon, Google, Meta, Microsoft, OpenAI, Oracle, and xAI. The president stated: "They can build their own plant, they're going to produce their own electricity." Companies signing the pledge "will build, bring, or buy the new generation resources and electricity needed to satisfy their new energy demands, paying the full cost of those resources, whether by building or buying from new or otherwise additive power plants." The pledge points toward private or dedicated generation solutions as, at the very least, a bridge to hybrid solutions that are interconnected to the public grid.

A private grid would consist of one or even many generating plants, backup resources such as battery storage to ensure reliability, and advanced power electronics and controls to ensure specific power-quality characteristics needed by data centers or large industrial facilities (for example, holding voltage within a narrower band than typical utility service), along with transformers and internal power lines. In other words, a private grid replicates many of the same types of equipment found in a public grid but operates as a self-contained network not electrically connected to the public grid.

Allowing or even encouraging data centers and other large loads to develop their own private grids could help address several pressing problems. First, it could insulate other customers from potential rate increases associated with utilities building infrastructure to serve data-center loads. In a fully private grid that remains physically and electrically separate from the broader system, none of the direct costs of generation or its related infrastructure could be allocated to the broader public grid and its customers. (The increased demand for the necessary equipment and labor could certainly increase prices, but that is true regardless of whether increased demand for electricity is driven by data centers, electric vehicles, or an expanding population.)

Second, establishing a private grid could enable large loads to avoid or streamline many of the regulatory requirements that apply to traditional electric utilities, which often slow infrastructure development. For example, environmental groups frequently advocate for aggressive energy conservation measures and investments in renewable resources as preferred or least-cost alternatives. Regulators and some state legislatures have prioritized policies that require or strongly encourage utilities to reduce peak demand and overall consumption before approving new infrastructure investments.

Although a physically separate grid for a large load could allow for more rapid development of the necessary generating resources and accompanying infrastructure, it does not solve all upstream supply-chain and fuel-delivery issues. Many data centers plan to rely on natural gas-fired generators for reliable, dispatchable power. But those require interconnection with a capable local gas distribution system or-more likely for large-scale projects-direct interconnection to an interstate gas transmission pipeline, along with negotiated transportation rates. Serving such loads at scale will likely require expanding the capacity of the interstate natural gas transmission system, which some states-particularly in the Northeast-have resisted due to concerns over greenhouse gas emissions and alignment with decarbonization goals. Moreover, increased reliance on gas-fired generation can mean greater vulnerability to changes in gas markets.

Developing a private grid (at least initially) would require a data-center operator to function, in effect, with its own vertically integrated electric provider. However, because power infrastructure is not a core competency for most large load developers, they will likely prefer to partner with experienced companies, including electric utilities, industrial firms, or specialized equipment manufacturers. For example, major industrial companies such as Chevron Corporation have long operated substantial on-site generation at their refineries. Similarly, in May 2025 Google signed an agreement with Elementl Power to build three 600 MW nuclear plants by 2035 to power its data centers.

Although on-site generating plants can eliminate direct impacts on other customers' electric rates, private grids raise important reliability considerations. As previously discussed, the rationale for developing power pools and RTOs was to reduce the risk of outages for individual participants by sharing backup generation across a larger, diverse system. To achieve comparable redundancy, private grids will need to install high-cost battery storage and/or build additional dispatchable generating capacity to serve as reserves-technically feasible, but at significant cost.

A hybrid solution offers another option under discussion. In this model, large loads build on-site power generation and also interconnect with the public grid-either initially or after approvals are secured-for backup and, potentially, to help meet peak demand on the public grid. Such arrangements involve significant complexities to ensure that they do not inadvertently raise rates for other customers. For example, many costs associated with operating RTOs are socialized across all users because it is often impossible to attribute specific causes, such as the system-wide expenses of maintaining voltage and frequency within established bounds. In states where COS regulation prevails, adding load can result in lower per-unit costs for existing customers by spreading fixed infrastructure expenses over expanded sales volume.

Whether large loads are met through public or hybrid grid solutions, the unprecedented scale and speed of demand growth are creating new reliability challenges that NERC is actively examining. NERC's March 2026 white paper concluded that existing reliability standards "are inadequate for the reliable integration of emerging large loads" onto public grids. Its efforts to address the grid impacts of large loads are expected to continue. Meanwhile, data centers are being built and planned at a pace exceeding the development of the infrastructure needed to accommodate them.

Another issue for interconnected generating plants serving data centers arises if the data center closes or significantly curtails operations, leaving its dedicated generation (whether on-site or under contract) no longer needed. If that generation is subsequently connected to the public grid, it may raise stranded cost issues reminiscent of those encountered during the early days of electric utility restructuring. In that era, utilities faced the question of who would bear the remaining book-value costs of plants built to meet their obligation to serve, after market prices fell below those costs. (Under COS regulation, utilities earn a return on the un-depreciated book value of their capital assets.) Similar allocation challenges could emerge today as wind and solar facilities are decommissioned.

Perspective

Data centers and other large loads have become convenient targets to blame for recent increases in electricity rates. That attribution is both overstated and counterproductive. Nevertheless, data-center growth is clearly a significant driver of rising electricity demand.

The rising data-center resistance movement advocates for banning or strictly limiting new data-center construction as the primary solution to our growing power challenges. Such measures have been proposed or advanced in numerous U.S. states and several European countries. In Europe, this stems partly from insufficient generating and grid capacity to accommodate rapid load growth alongside commitments to intermittent renewables as a means to meeting net-zero goals and partly because of physical concerns, such as water usage, and general concerns about Big Tech, including social-media harms, AI-driven job displacement, and privacy issues. Along similar lines, legislation recently introduced in Congress calls for a moratorium on new data-center development until safeguards address not only higher electric rates but also increased carbon emissions, water consumption, and privacy risks.

But limiting or banning data centers is ultimately self-defeating. Attempting to restrict technological advances in one location simply shifts those investments, jobs, and capabilities elsewhere. Europe is a clear example of this phenomenon, as traditional industrial facilities-from automobile manufacturers to chemical plants-are closing down.

Large loads that develop fully private grids with no physical connection to the public grid will self-evidently bear the full cost of their power needs. By avoiding the lengthy interconnection requirements and contentious debates over cost allocation, such facilities can be built and brought online more quickly. This approach benefits society overall and protects consumers from rate increases. Many view fully separate private grids as a practical first step toward hybrid solutions. Speedy interconnections to public grids, where possible, can benefit both large loads and the grid itself.

For now, however, surveys show that a significant share (20%-50%) of forecast data centers plan to pursue some form of private grid solution. Ultimately, the mix of private, hybrid, or traditional public-grid approaches will depend largely on how quickly and effectively regulators at state and federal levels reform the complex approval processes required for connecting large loads to the public grid and, collaterally, for building or connecting new generation sources.

Whether by additions to the public grid or as a series of private grids, America has the ability to make and install electric equipment that will power the nation into a secure and prosperous future. We must demonstrate the collective will to meet the challenge.

Notes

International Energy Agency (IEA), Electricity 2026 (IEA, 2026).

Bank of America Institute, Power Check: Watt's Going On with the Grid? (Bank of America Institute, 2025).

PJM Resource Adequacy Planning Department, 2026 PJM Load Forecast Report (PJM, 2026). PJM expects load to grow over 50% in the mid-Atlantic states by 2035 and expects peak demand to double.

Elliott J. Nethercutt, Demand Flexibility Within a Performance-Based Regulatory Framework (National Association of Regulatory Utility Commissioners, 2023).

North American Electric Reliability Corporation (NERC), 2025 Long-Term Reliability Assessment (NERC, 2026), 7.

"Fact Sheet: President Donald J. Trump Advances Energy Affordability with the Ratepayer Protection Pledge," The White House, released March 4, 2026, https://www.whitehouse.gov/fact-sheets/2026/03/fact-sheet-president-donald-j-trump-advances-energy-affordability-with-the-ratepayer-protection-pledge.

Data Center Watch, $64 Billion of Data Center Projects Have Been Blocked or Delayed amid Local Opposition (Data Center Watch, 2025).

See, for example, 16 U.S.C. Section 824d(a).

Tom Banse, "Demolition of Last Northwest Aluminum Smelter Signals End of an Industrial Era," Washington State Standard, March 6, 2026.

"Understanding Wholesale Capacity Markets," Federal Energy Regulatory Commission (FERC), last updated June 16, 2025, https://www.ferc.gov/understanding-wholesale-capacity-markets. A capacity market can best be thought of as an administrative construct that relies on bids to provide generation owners with money for keeping "iron in the ground." It also provides additional revenues for generators, especially peaking plants, that would otherwise not obtain sufficient revenues from selling electricity in the wholesale market to recover their costs. Under traditional utility regulation, the full costs of those plants would be recovered through rates.

"Net Generation," Electricity Data Browser, EIA, accessed April 20, 2026, https://www.eia.gov/electricity/data/browser.

Two seminal U.S. Supreme Court cases established this regulation: Bluefield Water Works & Improvement Company v. Public Service Commission of West Virginia, 262 U.S. 679 (1923); and Federal Power Commission v. Hope Natural Gas Company, 320 U.S. 591 (1944).

"About PJM," PJM, accessed April 20, 2026, https://www.pjm.com/about-pjm.

Sam H. Schurr and Bruce C. Netschert, Energy in the American Economy, 1850-1975: An Economic Study of Its History and Prospects (Johns Hopkins University Press, 1960); "Table 1.1.6 Real Gross Domestic Product, Chained Dollars," National Data: National Income and Product Accounts, U.S. Bureau of Economic Analysis, accessed April 21, 2026, https://apps.bea.gov/iTable/?reqid=19&step=3&isuri=1&categories=survey&nipa_table_list=6&Series=A&select_all_years=1; and Mickey Francis, "How Has U.S. Energy Use Changed Since 1776?," Today in Energy, EIA, July 2, 2025.

Jonathan Lesser, "The Used and Useful Test: Implications for a Restructured Electric Industry," Energy Law Journal 23 (2002): 349-81.

The National Energy Act, which was passed in response to the 1973 OPEC oil embargo, comprised five separate legislative acts addressing energy conservation, renewable energy development, industrial fuel use, natural gas use, and energy taxes.

Public Utility Regulatory Policies Act of 1978, Public Law 95-617, 92 Stat. 3117 (November 9, 1978).

Powerplant and Industrial Fuel Use Act of 1978, Public Law 95-620, 92 Stat. 3289 (November 9, 1978).

California Public Utilities Commission (CPUC), "Order Instituting Rulemaking on the Commission's Proposed Policies Governing Restructuring California's Electric Services Industry and Reforming Regulation," R.94-04-031 (April 20, 1994).

Electric Utility Industry Restructuring Act, Cal. Assem. B. 1890, 1995-96 Reg. Sess., ch. 854 (approved September 23, 1996).

Severin Borenstein, "The Trouble with Electricity Markets: Understanding California's Restructuring Disaster," Journal of Economic Perspectives 16, no. 1 (Winter 2002): 191-211.

Christopher Weare, The California Electricity Crisis: Causes and Policy Options (Public Policy Institute of California, 2003).

Han Hwang, "Regulated vs. Deregulated Electricity: Market Guide 2026," Energy Blog, ElectricRates.org, December 8, 2025.

Energy Policy Act of 1992, Pub. L. No. 102-486, 106 Stat. 2776 (1992).

"Promoting Wholesale Competition Through Open Access Non-Discriminatory Transmission Services by Public Utilities; Recovery of Stranded Costs by Public Utilities and Transmitting Utilities," Order No. 888, 61 Fed. Reg. 21,540 (May 10, 1996), FERC Stats. & Regs. 31,036.

Regional Transmission Organizations, Order No. 2000, 65 Fed. Reg. 809 (Jan. 6, 2000), FERC Stats. & Regs. 31,089 (1999), 18 C.F.R. pt. 35.

"Transmission and Power Markets," Nicholas Institute for Energy, Environment & Sustainability, Duke University, accessed April 13, 2026, http://nicholasinstitute.duke.edu/issues/transmission-and-power-markets.

"About PJM."

Kira R. Fabrizio, Nancy L. Rose, and Catherine D. Wolfram, "Do Markets Reduce Costs? Assessing the Impact of Regulatory Restructuring on U.S. Electric Generation Efficiency," American Economic Review 97, no. 4 (September 2007): 1250-77; Jeff Lien, Electricity Restructuring: What Has Worked, What Has Not, and What Is Next, EAG Discussion Paper EAG 08-4 (Antitrust Division, U.S. Department of Justice, 2008); and Steve Cicala, "Imperfect Markets Versus Imperfect Regulation in U.S. Electricity Generation," American Economic Review 112, no. 2 (February 2022): 409-41.

NERC, Glossary of Terms Used in NERC Reliability Standards (NERC, 2026), s.v. "Adequacy."

The term synthetic is used here because no such market mechanism would develop independently.

Hailong Hui et al., "Reliability Unit Commitment in the New ERCOT Nodal Electricity Market," paper presented at 2009 IEEE Power & Energy Society General Meeting, Calgary, AB, Canada, 2009. ERCOT and the California ISO, for example, use reliability unit commitment.

Monitoring Analytics, LLC, "Section 5: Capacity," in 2025 State of the Market Report for PJM, Volume 2: Detailed Analysis (Monitoring Analytics, LLC, 2026).

Jason McGovern, "What Happens When an Owner Wants to Close Its Power Plant?," PJM Inside Lines, June 11, 2019. RTOs can request that generators needed for reliability continue operations and be compensated on a COS basis, including a return on investment. Although RTOs can request that generation owners enter into such reliability-must-run agreements, they cannot compel generators to do so.

Surin Maneevitjit et al., "The Evolution of Capacity Markets in the USA," paper presented at the 6th International Conference on the European Energy Market, Leuven, Belgium, May 27-29, 2009.

Miguel Yanez-Barnuevo, "Data Center Power Demands Are Contributing to Higher Energy Bills," Environmental and Energy Study Institute, February 24, 2026.

Jonathan Lesser, What's Driving Higher Retail Electric Rates? (National Center for Energy Analytics , 2025); and Ryan Wiser et al., "Factors Influencing Recent Trends in Retail Electricity Prices in the United States," The Electricity Journal 38, no. 4 (December 2025): 107516.

See, for example, Dan Swinhoe, "Google, Tesla, Carrier Form New Lobbying Group Focused on U.S. Grid Capacity," Data Center Dynamics, March 11, 2026. The three companies announced the formation of a new lobbying coalition called Utilize to address what they term the "underutilization" of the public grid. Rather than offer a new approach, this organization will emphasize continuing the same strategies for meeting increasing demand.

Associated Press, "Read the Complete Transcript of Trump's 2026 State of the Union," AP News, February 25, 2026.

The White House, "Ratepayer Protection Pledge," press release, March 4, 2026.

"Act to Allow for Consumer Regulated Electric Utilities," American Legislative Exchange Council (ALEC), finalized January 6, 2026, https://alec.org/model-policy/act-to-allow-for-consumer-regulated-electric-utilities. ALEC has prepared model legislation to create consumer-regulated utilities that could not sell power to residential consumers and would be physically unconnected to public utility systems.

Jamie Dickerson and Kyle Murray, "Why New England Must Say No to New Gas Pipelines," Acadia Center, February 18, 2026; and Cy McGeady and Bridgette Schafer, "Navigating the Climate and Energy Implications of a Northeast Pipeline," Center for Strategic & International Studies, April 16, 2025.

Dan Yurman, "Google Plans Three 600 MW Nuclear Projects for Data Centers," Neutron Bytes (blog), May 7, 2025.

There can be indirect impacts. For example, building new gas-fired generators increases the demand for natural gas, which can lead to higher natural gas prices for all gas-fired generators. Similarly, increased demand for transformers can increase their prices, etc.

NERC, Assessment of Gaps in Existing Practices, Requirements, and Reliability Standards for Emerging Large Loads, NERC Large Loads Working Group White Paper (NERC, 2026).

"Large Loads Action Plan," NERC, last modified March 20, 2026, https://www.nerc.com/initiatives/large-loads-action-plan.

Curtis Schube and Mark P. Mills, Who Pays When Wind Turbines and Solar Panels Wear Out? A Hidden Energy Liability (NCEA, 2025).

Data centers have also become lightning rods for broader fears about the effects of artificial intelligence and Big Tech on society.

Christina Beatty and Steve Fothergill, "The Long Shadow of Job Loss: Britain's Older Industrial Towns in the 21st Century," Frontiers in Sociology 5 (August 2020): article 54.

Julia Shapero, "Sanders, Ocasio-Cortez Unveil Bill to Halt Data Center Construction," The Hill, March 25, 2026.

Dominik A. Leusder, "German Deindustrialization Is Self-Inflicted," Jacobin, March 5, 2026.

FERC, "Energized for 2026," press release, January 14, 2026.

Mark P. Mills, "Americans Shouldn't Have to See Data Centers on Their Electricity Bill," Opinion, Washington Post, March 23, 2026.

Continue Reading

-2%20(5).png)

Unreasoned Decisionmaking: FERC's Ever-Changing Methodology for Estimating the Return On Equity

The financial crisis that began in 2008 led to unprecedented actions by the U.S. Federal Reserve (Fed) to lower interest rates and stimulate the economy.

The SEC's Climate Rules Will Wreak Havoc on U.S. Financial Markets

The final climate disclosure rules issued by the Securities and Exchange Commission (SEC) in March 2024 will require every large U.S. corporation to report in detail all the climate-related physical and transition risks faced by their businesses, along with the direct and indirect greenhouse gas emi