Energy Sanctions as a Foreign Policy Tool: How Successful and for How Long?

Listen to the Brief

The Issue

Energy sanctions are a key foreign policy tool for the United States, most visibly deployed in geopolitical hot spots in Europe, Venezuela, and Iran. What are the results thus far of these sanctions? Will U.S. energy sanctions be viable for the long-term, given high resource depletion rates for shale and growing competition for energy by new actors, such as artificial intelligence (AI)? This issue brief addresses these questions.

At present, the U.S. energy resurgence reduces a historical overdependence on foreign oil and affords the U.S. government an enhanced ability to use targeted energy sanctions as a foreign policy tool. The U.S. Energy Information Administration (EIA) reports that the United States produced a record amount of all forms of energy in 2024, exceeding 103 quadrillion British thermal units.1 In 2025, the United States was also the world’s largest exporter of liquefied natural gas (LNG) and the first country to export over 100 million metric tons of LNG annually.2 This surging energy output, of which oil and gas account for 65%, reduces vulnerability to foreign energy shocks in a way that is unimaginable to those who recall the Organization of Arab Petroleum Exporting Countries (OAPEC) oil embargoes of the 1970s.3 America’s energy abundance allows for energy sanctions to be a viable policy option today, even against some of the world’s largest energy-producing countries, such as Russia, Venezuela, and Iran.

The Reality

What Are Energy Sanctions, and Are They Working?

The United States currently has the diplomatic ability to impose unilateral—and, with allies, to join multilateral—energy sanctions efforts on a range of countries, people (i.e., Specially Designated Nationals), and companies. U.S. sanctions are usually issued by the executive branch through executive orders (EOs) and, less often, by congressional legislation. Sanctions “prohibit, limit, condition, or regulate certain economic activities” and are implemented, interpreted, and enforced by the executive branch.4

Russia

U.S. energy sanctions on Russia began in 2014 in the wake of the occupation of Crimea, initially restricting financial access by certain Russian energy firms and limiting Russia’s access to new oil exploration and production technology for Arctic offshore, deepwater, and shale oil projects.5 On March 8, 2022, shortly after Russia’s war on Ukraine began, EO 14066 was signed, barring U.S. imports of Russian crude oil, petroleum fuels, refined products, LNG, coal, and coal products.6The EO also prohibits new investments in Russia’s energy sector by a U.S. person, as well as any financing, facilitation, or guarantee for Russian energy investments by a U.S. person, wherever located. A G7 Price Cap Coalition, which also includes Australia, imposes a price ceiling on Russia’s maritime oil exports in an effort to limit Russia’s energy sector revenues. The European Union (EU) has now imposed 19 sanctions packages on the Russian energy sector.7 In October 2024, the United States and the EU significantly tightened overall sanctions on Russian energy flows. The United States directly sanctioned Russia’s two largest oil companies, creating secondary sanctions risk for the Asia-Pacific region refiners that import Russian oil. The EU also moved to deepen sanctions on two major Russian oil firms and to impose additional sanctions on a shadow fleet of tankers that use deceptive practices to help Russia evade these sanctions.8

The EU now bans the import of spot cargoes of Russian LNG. Russian gas supplied by pipeline to the EU will be prohibited in 2027.9 Europe is currently America’s largest LNG market. U.S. LNG exports to Europe of 6.3 billion cubic feet per day (bcf/d) in 2024 have more than doubled since 2019 and now represent more than half of all U.S. LNG exports.10 U.S. LNG backstops Europe’s efforts to impose energy sanctions and helps shield Europe from Russia’s energy coercion. The EIA reports that Russia’s share of natural gas exports to Europe fell by more than two-thirds, from 14 bcf/d in 2020 to 4.4 bcf/d in 2024, as American supplies provided a ready replacement.11 Years of bipartisan energy diplomacy with the EU are also providing greater energy independence for the Mediterranean and the Balkans. The Vertical Gas Corridor, which links a Greek floating storage and regasification ship to the Trans-Balkan pipeline, allows U.S. LNG to serve as an economic alternative to Russian gas supplies in landlocked Central European states.12

In the crude oil sector, the port of Rotterdam is now the single largest export destination for U.S. crude oil.13 U.S. oil exports to Europe have surged since Russia’s war on Ukraine. In turn, this has helped backstop EU oil sanctions that largely bar Russian crude oil and refined product sales there.14

Sanctions Results?

The International Energy Agency (IEA) estimates that, in November 2025, a combination of lower oil exports, largely due to sanctions, and lower global oil prices reduced Russia’s monthly oil revenues to $11 billion—$3.6 billion lower than in 2024.15 Goldman Sachs reported in December 2025 that Russia’s oil export revenues fell by half in rubles, from 7.6% of GDP to 3.7%, and the Russian Ministry of Finance reported that oil and gas tax revenues fell by 34% year-over-year.16 Energy sanctions on Russia are assuredly reducing revenues, eroding Russia’s energy export markets and putting pressure on Putin’s government to negotiate an end to its brutal war on Ukraine.

Venezuela

Starting in 2005, the United States imposed sanctions on Venezuela, largely over antidemocratic, counternarcotics, and corruption concerns.17 In 2019, EO 13850 directly sanctioned Venezuela’s national oil company, PdVSA, freezing property and interests subject to U.S. jurisdiction and prohibiting U.S. persons from engaging in transactions with the company.18 Since then, the U.S. Department of the Treasury’s Office of Foreign Assets Control (OFAC) has issued a series of amended licenses to allow limited transactions for a small number of energy firms to produce petroleum and natural gas in Venezuela. On December 15, 2025, President Trump announced a blockade of “sanctioned oil tankers” transporting oil or oil products to and from Venezuela.19 While Venezuela exported on average 950,000 barrels per day (b/d) in November 2025, the blockade effectively deterred sanctioned and unsanctioned tanker traffic, cutting exports by half by the last week of December 2025.20 In the wake of the January 3 arrest of Nicolás Maduro, U.S. Secretary of State Marco Rubio underscored that sanctions and the blockade will continue to be instrumental in managing the relationship with the interim authorities in Venezuela. As part of that process, U.S. Secretary of Energy Chris Wright is overseeing a program of tendering Venezuela’s oil, controlling and disbursing energy revenue flows to help meet the needs of the Venezuelan people during this time of transition.21 OFAC’s January and February 2026 General Licenses 46–50 now permit the return of U.S. energy sector trade and investment as part of overall diplomatic efforts to restore democracy in Venezuela.

Sanctions Results?

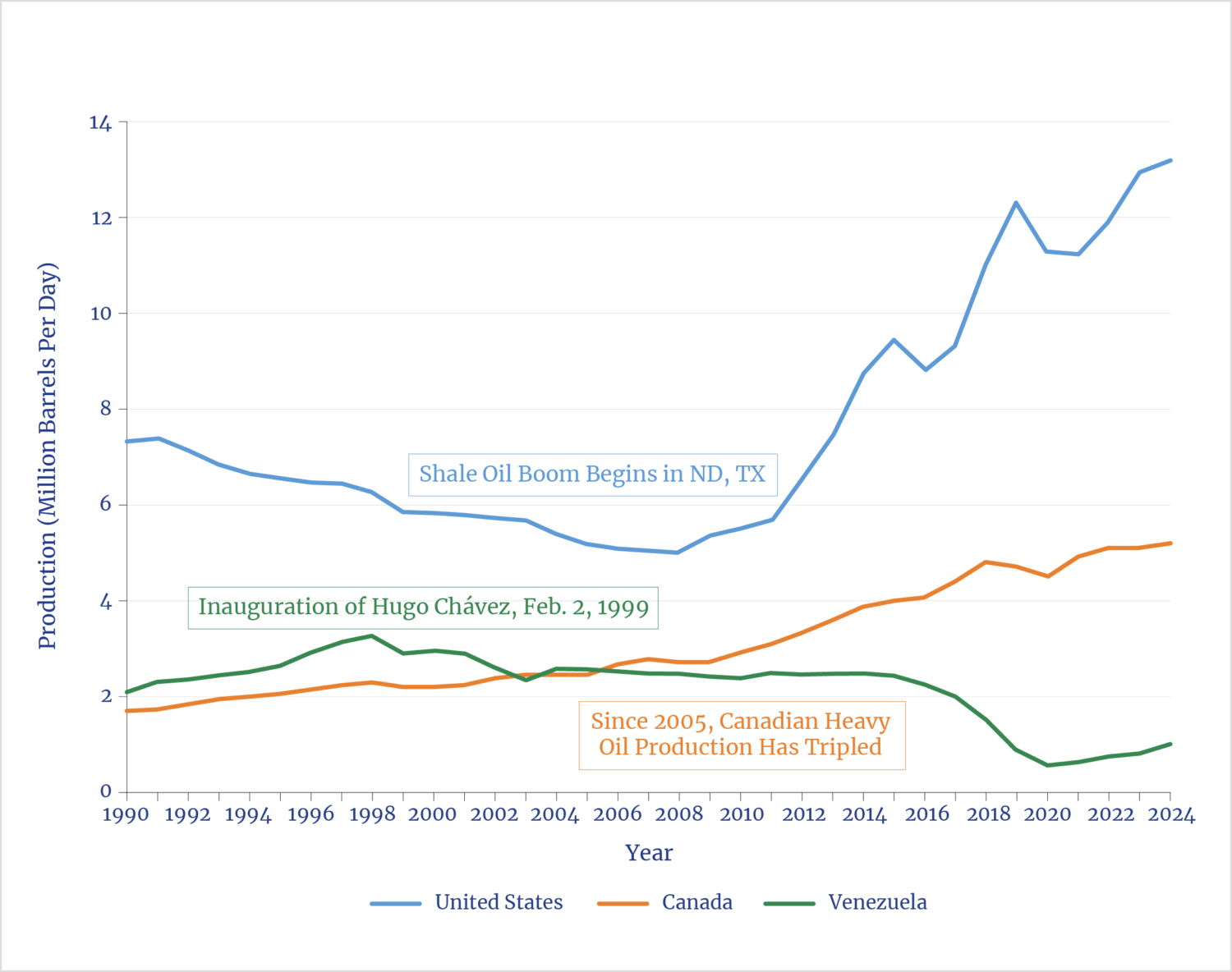

Venezuela was consistently among the largest suppliers of foreign oil to the United States, with exports peaking in the 1990s.22 Venezuelan oil policy changed decisively with Hugo Chávez’s inauguration in 1999, leading to increases in taxation on foreign oil companies and nationalizations, both of which contributed to lower overall production and exports to the United States. This period coincided with sharp increases in the flow of Canadian heavy oil to the United States and booming U.S. shale oil production. Both developments provided effective substitutes for Venezuelan oil in the U.S. market. In turn, this afforded U.S. administrations of both parties the ability to deepen U.S. sanctions on Venezuela. Reduced Venezuelan energy production, exports, and revenues stemming from the overall deterioration in the country’s investment climate, combined with direct sanctions on the oil sector starting in 2019, greatly increased pressure on Venezuelan authorities. A strong suite of sanctions, combined with the unimpeded arrest of Maduro, left Venezuela’s interim authorities with little choice but to cooperate with the United States. In many ways, it was the surging oil production of the U.S. Permian Basin that reduced the economic costs of ever stricter U.S. sanctions on Venezuela, ultimately helping to backstop military and diplomatic efforts that have facilitated the release of hundreds of political prisoners from the notorious El Helicoide prison and triggered the ongoing process for political change. A representation of these key energy production milestones is shown in figure 1.

Figure 1. Oil Production from 1990 to 2024 in Canada, the United States, and Venezuela, with Key Milestones

Iran

In the case of Iran, the United Nations (UN) and the United States imposed sanctions over nuclear proliferation, terrorism, and human rights concerns. The UN and targeted U.S. sanctions impede Iran’s ability to earn hard currency from oil sales. In August 2025, the UN “reimposed sanctions and other restrictions pursuant to six UN Security Council Resolutions—1696, 1737, 1747, 1803, 1835, and 1929—based on Iran’s continuing ‘significant non-performance’ of its nuclear commitments.”23 U.S. executive branch restrictions on Iran’s oil sector date back to the Iran hostage crisis of 1979. Congress deepened sanctions on the Iranian energy sector through Section 1245(d) of the fiscal year 2012 National Defense Authorization Act (P.L. 112-81; 22 U.S.C. §8513a(d)), which “directs the President to block from the U.S. financial system foreign financial institutions that knowingly conduct ‘any significant financial transaction’ with sanctioned Iranian banks, including Iran’s Central Bank.”24 At the start of the second Trump administration, National Security Memorandum (NSM) 2 from February 4, 2025 tightened energy sanctions further and “directs the imposition of maximum pressure on the Iranian regime to deny access to resources needed to sustain its destabilizing actives.”25 On November 20, the Treasury Department implemented NSM 2 partly by “sanctioning a network of front companies and shipping facilitators that bankroll the Iranian armed forces by selling crude oil.”26

Sanctions Results?

Taken together, multilateral and U.S. sanctions on Iran, combined with falling global oil prices and the increasing costs of exporting oil to Asia at a discount as high as $11 per barrel of crude oil, have sharply reduced oil’s contribution to Iran’s federal budget.27 Moreover, the IEA reported at the end of 2025 that Iranian oil stored at sea due to a decrease in Chinese refinery purchases had risen by 40 million barrels since August, imposing additional transaction costs on Iranian exporters.28 These expanded sanctions increased internal pressure for change on the Iranian regime, as seen by recent and widespread demonstrations within the country. These sanctions have also brought U.S. and Iranian diplomats together for rare in-person negotiations.

The Shadow Fleet

An inconvenient reality in the energy sanctions space is the use of maritime deception tactics by Russia, Venezuela, and Iran. Numerous rounds of U.S. and 19 formal packages of EU sanctions and enforcement actions have limited the ability of sanctioned states and companies to work around sanctions programs through falsely registered shadow fleet tankers. S&P Global and Lloyds estimate that nearly 1,000 to more than 1,400 tankers are now in the shadow fleet, making up almost 20% of global tanker capacity.29 Hundreds of tankers have been sanctioned by the United States alone, along with captains and other intermediaries.30 The impact of these actions is seen in the fluctuation in tanker rates. Responding to vigorous sanctions packages by the United States on both Iran and Russia, charter rates for very large crude carriers from the Middle East to China increased by 576% last year.31 Washington and Brussels correctly argue that increasing enforcement cuts yet further into illicit revenues for sanctioned suppliers, increasing their operational and insurance costs.

Sanctions have given rise to increasing amounts of floating oil stored at sea as buyers turn cautious, given the specter of secondary sanctions. Floating oil delays revenues for sanctioned states while increasing costs through ever higher daily tanker charter rates. This causes delays to accrue months beyond normal shipping times. Shadow fleet tankers often serve all three sanctioned countries. For example, on January 7, the U.S. Coast Guard seized the Marinera (formerly Bella 1) tanker in the North Atlantic Ocean after it fled Venezuelan waters, having been reflagged and renamed as a Russian vessel during its transit. The Bella 1 was initially sanctioned by the United States in 2024 for carrying illicit Iranian oil.32 The U.S. policy for maritime interdiction, seizing, deterring, and boarding suspected sanctioned tankers off Venezuela is, therefore, affecting the global shadow fleet overall.

How Long Can the U.S. Continue to Rely on Energy Sanctions?

Peak oil, or “Rumors of my death are greatly exaggerated”—Mark Twain

The ability to leverage energy as a foreign policy tool and deploy energy sanctions relies in large part on continued robust domestic oil and natural gas production. Much has been written about peak oil theory. Once again, there is increasing oil trade press about how long the United States can maintain record levels of oil output.33 The current discussion is driven by the reality that America’s oil and gas resurgence is a result of the development of shale resources, the recoverable reserves of which are now as low as 10% of the total resource base. This compares with at least 30% recovery rates for conventional oil deposits.34 To address this dynamic, energy companies, in partnership with the U.S. Department of Energy, are focused on increasing the recovery rate from existing shale structures through new technologies. As Bloomberg’s Javier Blas reports, “the next phase of the [shale] revolution—call it shale 4.0—is an engineering arms race to improve the so-called recovery factor.”35 Companies are using AI, new “propping technologies” to further open shale rock formations and to extend lateral drilling lengths, and are brewing new formulas of liquid surfactants to stimulate the flow of hydrocarbons from these structures. Current indications from oil majors, who are now the lead producers in the Permian Basin, are that these efforts are working.36 The Permian produces an astonishing 6.75 million b/d, which is more than the production of any OPEC country except Saudi Arabia. Overall, three U.S. states led 2025 oil production gains: oil production rose 240,000 b/d, or 11%, in New Mexico, which shares the Permian Basin with Texas; by 8% in Alaska, thanks to a new field on the North Slope; and by nearly 3% in Oklahoma, due to increases in hydraulic fracking in the state.37

Offshore, in federal waters, new ultra-deepwater technologies, linkages to existing gathering infrastructure, and regulatory incentives such as reduced royalty rates and steep increases in offshore lease availability are mobilizing significant new investments. These developments are reversing predicted declines in offshore production into overall increases. The EIA forecasts an increase in federal offshore production of 100,000 b/d to 1.81 million b/d (mb/d) for 2026.38 High-pressure drilling technology is already unlocking new deposits in exploration and production.39 Subsea tiebacks, from floating production units to existing seafloor infrastructure and pipelines, are making new projects more economical.40 The federal government is also offering new access to offshore tracks. The One Big Beautiful Bill Act mandates that the U.S. Department of the Interior hold some 36 offshore lease sales in the Gulf of Mexico and Alaska’s Cook Inlet by 2040. The first lease round was initiated on December 10, 2025, generating over $300 million for 181 blocks over 80 million acres.41 A second sale will be held in March 2026. The act also lowers the royalty rate from 16.67% to 12.5%.

Overall, for combined onshore and offshore crude oil production, the EIA forecasts that U.S. oil production will remain near its record high of 13.6 mb/d in 2026 and decrease slightly to a still-robust 13.3 mb/d in 2027.42 The innovative technology being deployed in the shale sector, combined with higher-pressure drilling and infrastructure tiebacks offshore, is good news for American energy security—and an inconvenient truth for OPEC and for those facing energy sanctions. The reality is that America’s foreign policy will benefit from the investments that companies are making in onshore and offshore technologies, coupled with additional access to offshore federal waters. Washington’s ability to impose oil sanctions on bad actors will continue well into the future.

Natural Gas, Canada and Mexico, and LNG

Natural gas production in the United States is at record levels and growing. In its February 2026 short-term energy outlook, the EIA revised its forecast for U.S. dry natural gas production to 110 bcf/d for 2026 and 111 bcf/d for 2027.43 The EIA forecasts that natural gas production overall will grow by 2% in 2026 and 1% in 2027.44 Natural gas production also benefits from the new technologies used for unconventional oil, particularly as much of the gas produced from the Permian structures is associated with oil production there.

The Natural Gas Supply Association estimates increases in associated gas from the Permian and Eagle Ford basins of 2.5 bcf/d in 2025.45 Gas trade within North America, which also has foreign policy benefits, remains robust. Natural gas flows in both directions to and from Canada, with U.S. gas exports important for Ontario, and Canadian gas imports flowing into major trunk lines in the upper Midwest. On net, the U.S. imports 7 bcf/d from Canada and is expected to export 6.6 bcf/d to Mexico this winter.46 In December, the EIA forecast that U.S. LNG exports would rise to nearly 15 bcf/d for year-end 2025 and 16.3 bcf/d in 2026, up from about 12 bcf/d in 2024.47 The LNG sector also benefits from the integrated nature of gas trade with Canada and Mexico, which is important for access to Asia-Pacific markets. The EIA estimates that LNG export capacity in North America could double to 28.7 bcf/d in 2029 if current projects begin operations as anticipated.48 Regulatory inducements and energy diplomacy with Japan also make projects such as Alaska LNG economic, further linking America’s gas surplus to growing markets in Asia.49 Overall, the EIA’s Annual Energy Outlook 2025 forecasts relatively high production growth of natural gas through 2030 and growing LNG exports through 2040 in most of its base cases.50 These developments support the ability of the United States to continue to impose natural gas and LNG-related sanctions on Russia and other sanctioned states.

Gas for Data Centers Versus LNG Exports

It is true that the AI and data-center boom is introducing uncertainty into the electric power sector and, by extension, the ultimate disposition of growing natural gas supplies. The amount of electricity that will be needed for data centers is staggering. Given gas’s leading role in supplying dispatchable, baseload electric power, powering AI will create more than a ripple effect in the ultimate use of incremental natural gas production. A recent study on the topic by NCEA Executive Director Mark Mills helps illustrate the sheer scale of the gas that may be needed. To supply 55 gigawatts—a low-end estimate for AI data-center power needs—another 10 billion bcf/d in natural gas would be needed by 2030.51 That amount is in addition to the 15 bcf/d that is also needed to supply U.S. LNG facilities now being built.52 This example helps spotlight the reality that growing competition between end-use sectors for gas may alter the economics of specific LNG investments. While change is the only certainty in forward-looking energy sector forecasts, the resource base, the regulatory certainty, and rapid increases in drilling technology will all help fuel ample growth in LNG exports. These exports, in high- and low-case forecast scenarios, will continue to sustain the role of American LNG as a key foreign policy benefit for the United States.

PERSPECTIVE

The U.S. energy resurgence is a sea change for its economy and directly strengthens national security. American presidents were once at the mercy of OPEC producers, and foreign policy options were limited by crippling oil import dependence from unstable regions. This is no longer the case. Washington can now pursue foreign policy goals free of the constraints of energy insecurity and now has its own energy weapon to use as a diplomatic tool. This American energy freedom allows diplomatic alliances in the Middle East to transcend oil sales, empowers European allies to stand up to Russian energy coercion, and supports the restoration of democracy in our own hemisphere. As the use of energy sanctions as a foreign policy tool in Europe and in Venezuela shows, sanctions do not eliminate but likely reduce the need for kinetic force to achieve foreign policy goals. Moreover, while the stick of imposing sanctions conveys foreign policy benefits, so too does the carrot of ratcheting back energy sanctions when warranted. The calibrated adjustments to Venezuelan energy sanctions and careful control of energy revenues provide new non-kinetic options that policymakers are using to try to return that country to a democracy.

Given recent examples of energy policy’s centrality to foreign policy, congressional debates on this topic should more fully consider the international implications of sustaining U.S. energy abundance as a foreign policy advantage and not just a domestic issue. Legislators from both parties can be reminded that energy policy debates are no longer purely domestic and have important impacts on our national interests far beyond the water’s edge.

Endnotes

- Mickey Francis, “In 2024, the United States Produced More Energy than Ever Before,” Today in Energy, U.S. Energy Information Administration, June 9, 2025.

- Curtis Williams, “U.S. Sets New LNG Export Records in Banner Year Marked by New Capacity,” Reuters, January 2, 2026.

- Francis, “In 2024, the United States Produced More Energy.”

- Liana W. Rosen, U.S. Sanctions: Overview for the 119th Congress (Congressional Research Service, 2025).

- Exec. Order No. 13662, 31 CFR 589.203–205 (2014).

- Exec. Order No. 14066, 3 CFR 13625–13626 (2022).

- Council of the European Union, “19th Package of Sanctions Against Russia: EU Targets Russian Energy, Third-Country Banks and Crypto Providers,” press release, October 23, 2025.

- Daniel Boffey, “Shadow Fleet Ships Moving Sanctioned Oil Reflagged to Russia at Rising Rate,” The Guardian, January 8, 2026.

- Council of the European Union, “19th Package of Sanctions Against Russia.”

- Victoria Zaretskaya, “The United States Remained the Largest Liquefied Natural Gas Exporter in 2024,” Today in Energy, U.S. Energy Information Administration, March 27, 2025.

- Hilary Hooper and Justine Barden, “Russia’s Natural Gas and Coal Exports Have Been Decreasing and Shifting Toward Asia,” Today in Energy, U.S. Energy Information Administration, September 3, 2025.

- United States Energy Association, The Vertical Gas Corridor (United States Energy Association, 2025).

- U.S. Energy Information Administration, “U.S. Crude Oil Exports Reached a New Record in 2024,” Today in Energy, U.S. Energy Information Administration, April 20, 2025.

- Francis, “In 2024, the United States Produced More Energy.”

- International Energy Agency,Oil Market Report—December 2025 (International Energy Agency, 2025).

- Huileng Tan, “Russia Is Still Exporting Plenty of Oil—but Earning Far Less to Fund Its War on Ukraine,” Business Insider, December 4, 2025.

- Clare Ribando Seelke, Venezuela: Overview of U.S. Sanctions Policy (Congressional Research Service, 2025).

- Seelke, Venezuela.

- Michelle L. Price, “Trump Orders Blockade of Sanctioned Oil Tankers into Venezuela, Ramping Up Pressure on Maduro,” AP News, December 16, 2025.

- Reuters, “Residual Fuel Fills Venezuela’s Storage Tanks as Exports Cut to Minimum, Sources Say,” Reuters, December 31, 2025.

- Megan Messerly, Aiden Reiter, and James Bikales, “The U.S. Couldn’t Track Billions in Iraq. Now, It’s Controlling Venezuela’s Cash,” Politico, January 22, 2026.

- “U.S. Imports from Venezuela of Crude Oil and Petroleum Products,” Petroleum & Other Liquids, U.S. Energy Information Administration, released February 6, 2026.

- U.S. Department of State, “Completion of UN Sanctions Snapback on Iran,” press release, September 27, 2025.

- Jennifer K. Elsea, Liana W. Rosen, and Clayton Thomas, Iran’s Petroleum Exports to China and U.S. Sanctions (Congressional Research Service, 2025).

- “National Security Presidential Memorandum/NSPM-2,” Presidential Actions, The White House, last modified February 4, 2025.

- U.S. Department of the Treasury, “Treasury Tightens Sanctions on Iran’s Oil Network Supporting Its Military,” press release, November 20, 2025.

- Dalga Khatinoglu, “The Year in Review: Iran’s Deepening Economic Crisis,” Middle East Forum Observer, December 27, 2025.

- International Energy Agency, Oil Market Report.

- Max Lin, “Factbox: Shadow Fleet Expands to Maintain Sanctioned Oil Flows,” S&P Global September 3, 2025; and Boffey, “Shadow Fleet Ships.”

- Sam Chambers, “U.S. Targets Sprawling Iranian Shadow Fleet Network in Latest Sanctions Drive,” Splash247.com, November 21, 2025.

- Weilun Soon, “Tanker Rates Hit New High as Buyers Seek Non-Russian Oil,” Bloomberg, November 24, 2025.

- Lex Harvey, “What We Know About the U.S. Seizure of a Russian-Flagged Tanker,” CNN, January 8, 2026.

- Robert Rapier, “The Return of Peak Oil,” Oilprice.com, May 15, 2025.

- Ed Crooks, “Aiming for the Big Prize in U.S. Unconventional Oil and Gas,” Wood Mackenzie (blog), December 12, 2025.

- Javier Blas, “Shale Oil’s Next Revolution Should Worry OPEC,” Bloomberg, November 19, 2025.

- Ron Bousso, “Permian to Retain U.S. Oil Crown Even After Hitting Peak,” Reuters, December 11, 2025.

- Alton Wallace, “U.S. Oil Output Rose to Record High in September,” New Orleans CityBusiness, December 4, 2025.

- Eulalia Munoz-Cortijo, “Gulf of Mexico Oil and Natural Gas Production Expected to Remain Stable Through 2026,” Today in Energy, June 6, 2025.

- Arathy Somasekhar, “Improved Drilling to Boost Gulf of Mexico Offshore Oil Output as U.S. Onshore Growth Slows,” Reuters, October 15, 2025.

- Wallace, “U.S. Oil Output.”

- “OBBBA Oil and Gas Leasing Program,” Bureau of Ocean Energy Management, accessed December 19, 2025.

- “Short-Term Energy Outlook (February 2026),” U.S. Energy Information Administration, released February 10, 2026.

- “Short-Term Energy Outlook (February 2026).”

- “Short-Term Energy Outlook (February 2026).”

- Dena E. Wiggins, “Record Gas Production Gives U.S. Market Stability Even with Growing Demand,” The American Oil & Gas Reporter, December 2025.

- Wiggins, “Record Gas Production.”

- Andrew Topf, “U.S. Natural Gas Output and Demand to Smash Records in 2025,” Oilprice.com, December 10, 2025.

- Jordan Young, “North America’s LNG Export Capacity Could More than Double by 2029,” Today in Energy, U.S. Energy Information Administration, October 16, 2025.

- Michael Lynch, “The Risks Around the Alaskan LNG Project,” Forbes, July 25, 2025.

- U.S. Energy Information Administration, Annual Energy Outlook 2025 (U.S. Energy Information Administration, 2025).

- Mark P. Mills, The Rise of AI: A Reality Check on Energy and Economic Impacts (National Center for Energy Analytics, 2025).

- Mills, The Rise of AI.