The SEC's Climate Rules Will Wreak Havoc on U.S. Financial Markets

The final climate disclosure rules issued by the Securities and Exchange Commission (SEC) in March 2024 will require every large U.S. corporation to report in detail all the climate-related physical and transition risks faced by their businesses, along with the direct and indirect greenhouse gas emi

Executive Summary

- The final climate disclosure rules issued by the Securities and Exchange Commission (SEC) in March 2024 will require every large U.S. corporation to report in detail all the climate-related physical and transition risks faced by their businesses, along with the direct and indirect greenhouse gas emissions of their operations. These new rules are not designed to protect investors, correct a market deficiency, or lead to more informed investment decision-making. They are instead meant to discourage capital formation for certain high-emitting sectors and redirect investment away from oil, gas, and coal companies, thus retarding their business growth and shrinking their hydrocarbon production over time.

- The SEC rules are part of the federal government's coordinated climate plan, the latest in a series of regulatory attacks against the traditional energy industry by the current administration. By imposing a climate test on all issuing and investing companies - basically, every financial market participant in the U.S. - the agency's goal is to help force an energy transition by stigmatizing carbon-emitting industries in general and fossil fuel producers in particular. Defunding oil, gas, and coal companies - mainly through the bank loan and corporate bond markets - is meant to shrink the supply of domestic hydrocarbons, cut national emissions, and help achieve the climate targets set for the U.S. for 2030 and beyond.

- There is no evidence that economic growth can be decoupled from emissions or fossil fuels, which means that decarbonization - which the SEC's rules will abet and accelerate - will create a new form of systemic financial and economic risk. Decarbonized financial markets will be more volatile, riskier, and less diversified, with fewer investment choices. Since energy-consuming industrial, utility, and technology companies represent the lion's share of most benchmark U.S. stock and bond indexes, decarbonization will amplify the market's exposure to fluctuating energy prices. It would also place the U.S. at a competitive disadvantage versus China, India, and other developing countries, none of which is playing by the same climate rules.

- A growing reliance on renewable wind and solar power will destabilize the American electricity grid and increase electricity prices across the board. Constraining the domestic supply of oil and natural gas will mean higher energy prices; these prices ripple through the broader economy, since hydrocarbons are used to produce or transport most goods and services.

- The forced reduction in domestic oil and gas production will also shrink the U.S. economy, given the traditional energy industry's importance (7.6% of U.S. GDP in 2021). It will lead to significant job losses, given the size of the American energy workforce (24.1 million direct and indirect jobs in 2023). Not maintaining American energy independence by reinvesting in domestic fossil fuel production will also pose a risk to national security. The net effect will be a diminished U.S. economy in 2030, one marked by anemic growth, higher inflation, increased unemployment levels, and a hollowed-out domestic industrial base. This has been Germany's fate. That country's experience with decarbonization is a warning of what lies in store for the U.S. if the federal government continues down its current climate policy path.

- The SEC's climate disclosure rules have been challenged in the courts, mainly on the grounds that the rulemaking exceeds the agency's statutory authority. In April 2024, the SEC announced that it was voluntarily staying the implementation of its new rules, pending the completion of a consolidated judicial review by the U.S. Court of Appeals for the Eighth Circuit. The Supreme Court's recent decision in Loper Bright Enterprises v. Raimondo, Secretary of Commerce, which threw out the precedent of regulatory agency deference set in Chevron U.S.A. Inc. v. Natural Resources Defense Council, will provide an important tailwind for these legal arguments.

- The SEC's climate disclosure rules, in short, would fundamentally transform the agency from an objective market referee to an active and partisan political player. This is in direct contravention of its regulatory mandate to remain impartial and simply ensure full disclosure and fair dealing across well-functioning financial markets. By imposing an emissions standard on the financial markets, the SEC will also be picking corporate winners and losers and influencing asset pricing and financial market access. Effectively, the agency will be tilting the playing field away from traditional energy and other high-carbon-emitting sectors, which is an inversion - if not a perversion - of the SEC's regulatory function.

Introduction

Over the past several years, the environmental, social, and governance (ESG) movement has swept across Wall Street and the U.S. corporate sector, spurred on by a network of sustain- ability advocacy groups led by the United Nations. As the financial complement to the U.N.'s 2015 Paris Agreement and 2030 Sustainable Development Goals, ESG posits that a new set of subjective, nonfinancial factors should be used to drive corporate policy and investment decision-making, as opposed to the objective financial metrics used to date. Climate change is the highest-priority ESG issue, and decarbonization is the overriding sustainability goal, even though there is no empirical data showing that reducing greenhouse gas emissions will lead to better financial performance for individual companies or investors. Despite this glaring fiduciary problem, there are now Wall Street investors who regularly engage with the companies they invest in to ensure that these businesses are toeing the ESG line, partic- ularly regarding climate change.

Moral pressure has been very effective in spreading sustainability doctrine throughout the financial system, but climate change concerns still do not affect financial asset prices or relative value relationships in the markets. While clean energy investment flows continue to rise, the capital spigot for the fossil fuels industry has not been turned off - yet. Despite all the public support by businesses and the financial industry for the decarbonization agenda, there has been no discernible change in the cost of capital or market receptivity for traditional energy companies. Indeed, over the past two years, several major banks and investment firms have withdrawn from net-zero alliances and adopted a lower public profile regarding ESG.1 New York Post, Feb. 15, 2024. For most companies, climate and other ESG-related shareholder resolutions are regularly voted down during the annual general meeting season.

Since a voluntary approach has not achieved the climate objectives of the sustainable finance movement, financial regulators - mainly in Europe and North America - have begun to mandate climate and other ESG reporting by companies and investment firms. The European Union (EU) has taken the lead, with the passage of its Corporate Sustainability Reporting Directive2 and companion Sustainable Finance Disclosure Regulation.EC, 3Both disclosure requirements are meant to ensure business and investor compliance with the climate and sustainability goals of the European Green Deal4 and the EU Taxonomy.5 Despite wresting its sovereign status back from the EU in 2020, the United Kingdom has adopted similar climate-driven financial regulations post-Brexit - including its own Sustainability Disclosure Requirements.6

The U.S. government is now following suit. In March 2024, the Securities and Exchange Commission (SEC) finalized climate disclosure rules for all regulated companies subject to the reporting requirements of the Securities Act of 1933 (1933 Act) and the Securities Exchange Act of 1934 (1934 Act)7 - essentially, every registrant required to file a Form 10-K or 20-F. The new rules require that companies include detailed and audited disclosure in their annual SEC filings about the supposed physical and transition risks posed by climate change to their businesses, along with the amount of greenhouse gas emissions generated by their operations, both directly and indirectly. The rules reflect the Commission's view that climate change represents a financial risk for companies and an investment risk for market participants, thus posing a potential threat to the entire financial system.

The SEC has also justified its new rulemaking on the grounds that investors must be protected against false and misleading company claims about their ESG policies, particularly involving climate change. In March 2021, shortly after President Biden took office, the agency created a Climate and ESG Task Force to curb "greenwashing" across the U.S. capital markets, mainly by charging and fining offenders for misstatements, omissions, and material gaps in climate and ESG disclosure.8 The SEC rationalized its new rules as a necessary response to investor demand for more clarity around ESG market protocols.9

Climate-driven ESG is not like standard investment analysis, where data facilitate analysis and lead to a final investment decision. Instead, mandatory disclosure of carbon emissions and other nonfinancial sustainability metrics is overtly intended to pressure issuing and investing companies to modify their corporate and financial policies and set sustainability targets for their businesses - chief among which would be achieving net-zero emissions in line with the U.N.'s 2015 Paris Agreement and 2030 Sustainable Development Goals. The SEC, like its European counterparts, is now attempting to direct capital flows and achieve specific market outcomes based on a climate litmus test. But decarbonization-driven financial regulations will have adverse macroeconomic consequences and lead to increased systemic risk for the U.S. financial markets.

Climate-Related Physical Risks: It's Really About the Weather

The SEC's climate disclosure rules will force the management of all registered companies to act as meteorologists and report every conceivable weather impact to their businesses over exceedingly long investment horizons. These companies will be required to describe any climate-related physical risks that "have materially impacted or are reasonably likely to have a material impact" on the company's business strategy, results of its operations, or financial condition. The SEC defines physical risks as the actual or potential negative impacts of extreme weather events and changes in long-term weather patterns on a registrant, which is more accurately described as weather risks, both short-term (acute) and long-term (chronic).

Yet weather events such as hurricanes, tornadoes, floods, droughts, and even wildfires are all natural phenomena that move in both seasonal and longer-dated cycles over a span of decades. There is no credible science to distinguish between naturally occurring weather events and so-called climate-related natural disasters, or to attribute the severity of individual storms to the effects of man-made climate change.10

Slight changes in temperatures and sea levels are imperceptible and have no impact on business decision-making. By conflating weather risk with climate risk, the SEC will ensure that U.S. businesses default to a very detailed level of weather-related disclosure - both historical results and hypothetical forward projections - so as to not run afoul of the Commission. Companies subject to the SEC rules will need to report all capitalized costs, expenditures expensed, charges, and losses incurred (net of insurance recoveries) due to "severe weather events or other natural conditions," subject to very low minimum disclosure thresholds set at the greater of 1% or $100,000 for the income statement and $500,000 for the balance sheet.11 For perspective, the mean equity market value of the S&P 500 index of companies was $96.9 billion as of July 31, 2024.12

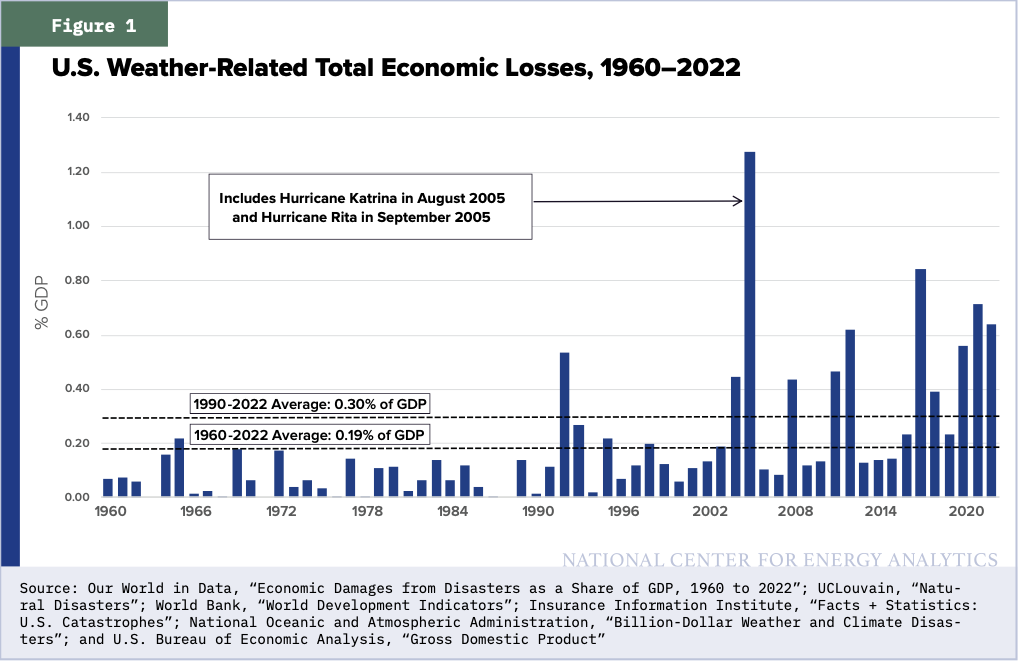

Weather risk remains a localized real estate problem. Historically, the costs of weather-related events or disasters have constituted a very small share of the U.S. economy while remaining readily manageable at the company level. U.S. weather-related economic losses, while increasing in nominal terms over time due to the combination of population growth, economic development, and general price inflation, continue to average well below 1% of annual gross domestic product (GDP) each year. As seen in Figure 1, such catastrophic losses (excluding earthquakes and volcanic eruptions) averaged only 0.19% of U.S. GDP over 1960-2022.13

At least since the 1980s, outsize weather events and active storm seasons have never spilled over into the broader markets. For example, in 2005, aggregate U.S. economic losses due to weather-related events amounted to $166 billion in 2005 dollars, the equivalent of a record 1.28% of GDP. In August of that year, Hurricane Katrina hit the eastern Louisiana coast, causing an estimated $125 billion in economic damage (most of which was due to engineering-related levee failures that led to the flooding of roughly 80% of low-lying New Orleans). This was followed four weeks later by Hurricane Rita, which made landfall on the western coast of Louisiana and caused $18 billion in estimated damage.

The combination of these two Category 3 hurricanes disrupted the entire Gulf Coast energy infrastructure system - including offshore oil and gas production and onshore storage and delivery - for nearly six months. Notably, roughly one-quarter of U.S. refining capacity was initially idled by the one-two- storm combo. Nevertheless, U.S. equity and credit markets performed strongly during the fourth quarter of 2005 and the first quarter of 2006, while U.S. real GDP growth averaged over 3% over the same six-month period. Between September 30, 2005, and March 31, 2006, the S&P 500 equity index traded up by 5.81%,14 and even the U.S. energy sector managed to eke out a positive equity market return of 1.35%.15 Similarly, U.S. investment-grade corporate bond spreads did not show any appreciable widening over the period.16

Weather-induced costs can potentially affect an individual company's operations and financial profile. However, such idiosyncratic, asset-specific company risk rarely rises to the level of industry, sector, or market risk and is already adequately captured in the general risk disclosures required in SEC filings. Most securities issuers subject to the reporting requirements of the 1933 and 1934 Acts are large corporations with geographically diverse businesses and global operations. Based on FactSet data during the second quarter of 2024, S&P 500 index member companies generated 41% of their aggregate revenues from outside the United States. By sector, the international revenue component ranged from Utilities (1% non-U.S.) and Real Estate (18%) at the low end to Industrials (33%) and Energy (39%) in the mid-range to Materials (53%) and Information Technology (57%) at the high end.17 For the majority of SEC filers subject to the Commission's climate rules, business scale and asset diversification render the issue of weather risk moot. Only a minority of SEC registrants - mainly, smaller companies in the startup phase - have highly concentrated geographic operations or single-asset profiles, neither of which has thus far presented a problem for the financial markets in terms of risk pricing or relative value investment analysis.

For example, Cheniere Energy, Inc., currently the largest U.S. liquefied natural gas (LNG) producer, with a 50% export market share in 2023, started out as a single-site project developer building a bidirectional facility at Sabine Pass in western Cameron Parish, Louisiana. Hurricane Rita tore a path through the region in 2005. Yet over the years 2006-17, the company was able to raise an aggregate $20.8 billion of capital from various markets (including bank loans, high-yield bonds, and public and private equity) to fund the construction of a regasification terminal, which changes LNG back to its original gaseous state (4.0 billion cubic feet per day capacity), and an initial four liquefaction trains, which change natural gas to a liquid state (18.0 million tonnes per annum capacity), at Sabine Pass, while continuing work on two additional trains.18

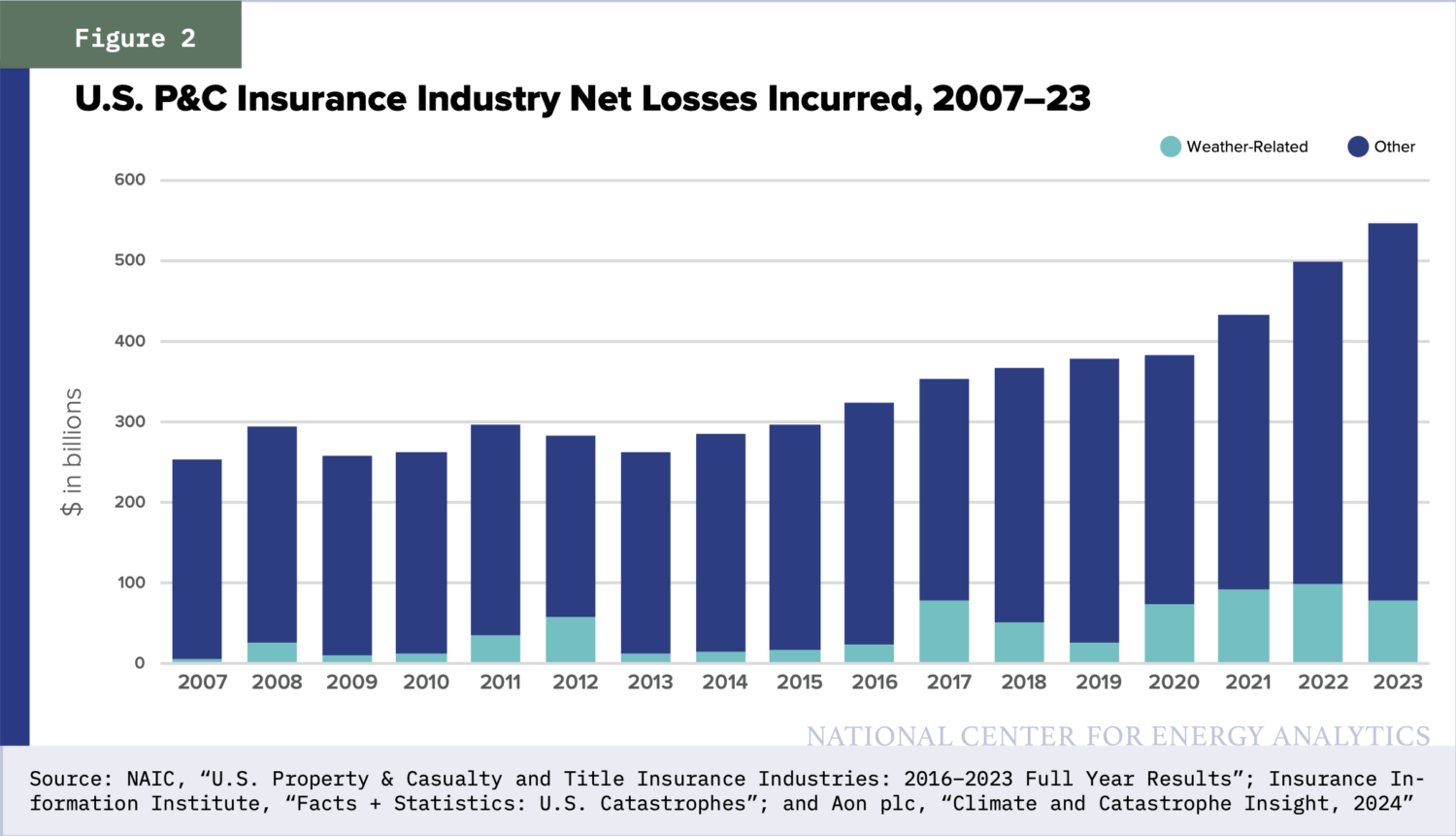

For companies with assets particularly exposed to weather variability, there are various tools that corporate executives can use to manage such risk. Chief among them is insurance - both casualty and business interruption - to protect against catastrophic loss and short-term disruptions in cash flow. To date, the U.S. property and casualty (P&C) insurance industry has been able to deal with any weather-related variability in its overall claims activity. As highlighted in Figure 2, based on data tracked by the National Association of Insurance Commisioners (NAIC) and the Insurance Information Institute, insured losses from weather-related events in the U.S. have remained a relatively small component of aggregate net losses incurred by the domestic P&C industry over the past two decades, never exceeding 20%-25% of the total, even during heavy storm years. Insured losses typically approximate 50%-60% of total storm-re- lated economic damages. While total weather-related economic losses averaged 0.37% of U.S. GDP over 2007-23, insured losses averaged only 0.21% of GDP. Moreover, this figure is further reduced when claims from personal homeowners and automotive policies (roughly 50%-60% of the total) are excluded to get a clean commercial loss number.19

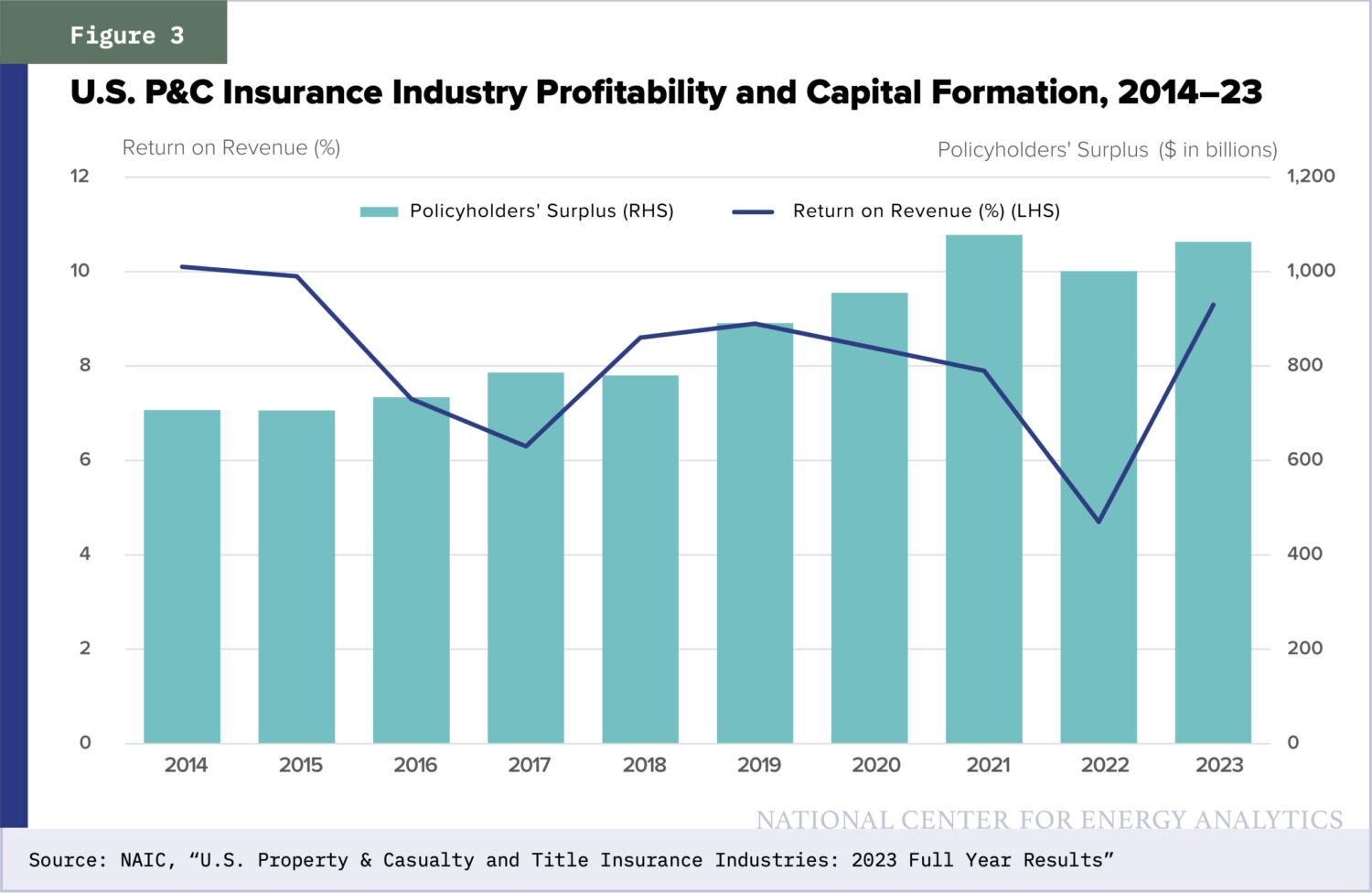

The fundamental profile of the U.S. P&C insurance industry remains strong despite increased losses in recent years, which have been mainly driven by higher inflation. Given the automatic premium-pricing adjustments that result when severe storms hit, the industry has a built-in defensive financial mechanism to insulate both its profitability and capital formation. Moreover, U.S. P&C insurers can also off-load a portion of their primary loss exposure using reinsurance ($562 billion global reinsurer capital as of year-end 2023) and alternative capital sources such as catastrophe bonds and other insurance-linked securities ($108 billion issued over 2002-23).20

Even with an uptick in annual insurance claims since 2014, industry underwriting profitability has hovered around the break-even mark on the back of continued strength in commercial business lines. Moreover, insurers' investment portfolio yields have remained positive despite a prolonged low interest rate environment since the 2008 global financial crisis - which is now reversing, pointing to improved investment returns going forward. The industry has been consistently profitable from a bottom-line perspective (9.3% return on revenue in 2023), which has allowed for the steady buildup of capital ($1.1 trillion policyholders' surplus as of year-end 2023), as seen in Figure 3.21 At year-end 2023, A.M. Best Rating Services, Inc. rated 96% of U.S. P&C insurance companies in either the "Good" or "Exceptional" category.22

In addition to insurance, companies can mitigate weather-related risk by locating new assets away from the locus of severe storms - Gulf and Atlantic Coasts for hurricanes, the Midwest and Great Plains region for tornadoes, California and other western states for wildfires - and by hardening physical infrastructure around existing facilities. In the Cheniere Energy example above, the company raised the elevation of its Sabine Pass critical process equipment by more than 18.5 feet above sea level in order to minimize the potential damage from any future hurricane storm surge.

Apart from a company's own risk management steps, investors can temper idiosyncratic weather risk by moving up in the capital structure (i.e., becoming a creditor rather than a shareholder) and lending on a secured priority basis at the asset level (i.e., standing first in line in the event of a catastrophic event). Bondholders have the option of taking out financial guaranty insurance to further guard against an interest or principal payment default. Debt and equity investors also may employ a seasonal strategy to actively trade investment positions in weather-exposed portfolio companies (e.g., avoiding storm-vulnerable names during the June through November U.S. hurricane season). For investors not comfort- able with analyzing or pricing weather risk for a particular company, the ultimate risk hedge would be not to have any corporate exposure at all.

Lastly, in terms of potential systemic risk, other types of natural disasters (such as earthquakes) and geopolitical factors (particularly military conflict) pose a much greater potential threat to American businesses and U.S. financial markets than weather events. Currently, the largest technology companies dominate the U.S. market: the Information Technology sector constituted over 30% of the S&P 500 index as of July 31, 2024,23 and the "Magnificent Seven" stocks - Alphabet Inc., Amazon. com, Inc., Apple Inc., Meta Platforms, Inc., Microsoft Corporation, NVIDIA Corporation, and Tesla, Inc. - accounted for roughly 60% of the equity market's total return in 2023.24 Given this reality, it's hard to imagine - never mind calculate - the costs (aside from human tragedies) from a major earthquake hitting Silicon Valley in northern California, which sits on the active San Andreas fault and is the headquarters location for most major U.S. technology companies.

Similarly, if armed hostilities were to break out between China and Taiwan, the implications for the U.S. economy and financial markets would be decidedly negative, given that Taiwan supplies roughly 60% of all semiconductors and 90% of the most advanced chips used by businesses globally.25 There are, in short, myriad credible and highly consequential risks that companies and their investors must grapple with, none of which the SEC dictates be documented and "disclosed" in such minute detail.

SEC Emissions Reporting: Placing a Bull's-Eye on Traditional Energy

By adopting carbon emissions as the "central measure and indicator of the registrant's exposure to transition risk"26 and the gauge for how companies are managing such risk, the SEC's goal is plain. The only way for issuers to reduce their transition risk is by shrinking their carbon footprint. For traditional energy companies, the only way to do this is by ceasing operations or going into a whole new line of business (green or otherwise). The Commission's rules spell out the various threats posed by

transition risks, all of which directly relate to the traditional energy industry. These include "increased costs attributable to climate-related changes in law or policy, reduced market demand for carbon-intensive products leading to decreased sales, prices, or profits for such products, the devaluation or abandonment of assets, risk of legal liability and litigation defense costs, competitive pressures associated with the adoption of new technologies, reputational impacts (including those stemming from a registrant's customers or business counterparties) that might trigger changes to market behavior, changes in consumer preferences or behavior, or changes in a registrant's behavior."27

What the SEC refers to as the risks associated with the transition to a lower-carbon economy are better described as political or regulatory risks. Moreover, the policies seeking an energy transition away from fossil fuels are being driven by politics, not by economics or market demand or shifting consumer preferences or technological advancements. To date, clean energy alternatives have been mainly forced on the market by government officials and regulators using a carrot-and-stick approach - subsidies of one kind or another to so-called renewable energy, on the one hand, and increasing restrictions and penalties on fossil fuels, on the other (see the Appendix, The Federal Full Court Press).

To make it easier for investors to target, isolate, and screen out companies with "large carbon footprints" (i.e., those producing or using large quantities of hydrocarbons), the new SEC rules require large corporations to disclose Scope 1 (direct) and Scope 2 (indirect upstream) greenhouse gas emissions if such emissions are material28 - which they clearly are, for the traditional energy sector. Under the reporting framework developed by the Greenhouse Gas (GHG) Protocol, Scope 1 emissions are defined as those generated by sources that are owned or controlled by a company (e.g., emissions from combustion by on-site boilers and furnaces or vehicles used in company operations), while Scope 2 emissions are those associated with the generation of purchased electricity consumed by a company (i.e., emissions that physically occur at the off-site facility where the electricity is generated).29 Based on Environmental Protection Agency (EPA) data, in 2022, the oil, gas, and coal industries generated 332 million tonnes of Scope 1 and 2 CO2 emissions, equivalent to 23% of the industrial sector total and 5% of the national total.30

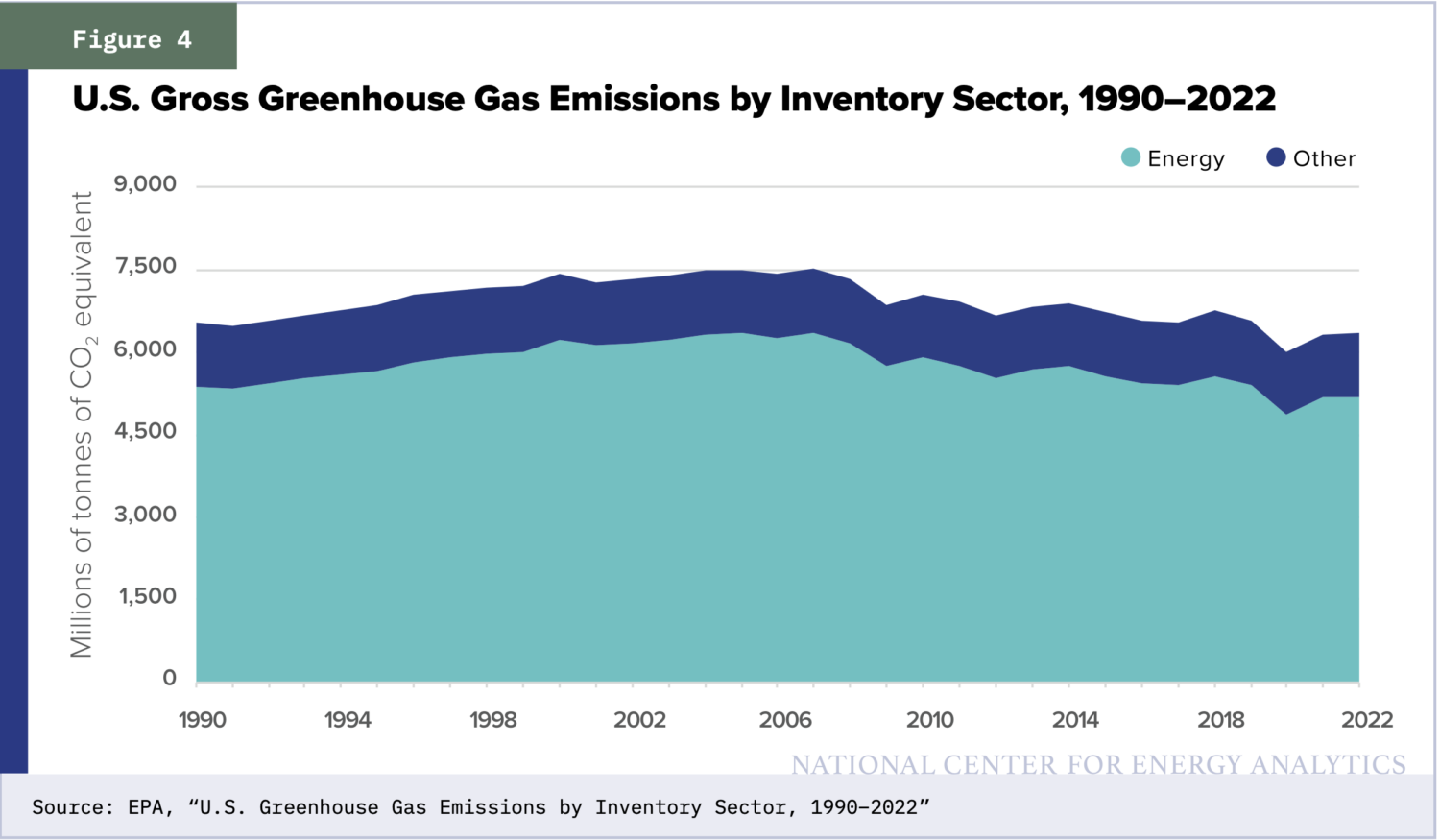

While the final rules do not mandate the disclosure of indirect downstream Scope 3 emissions, this concession does not change anything, since the fossil fuel industry is responsible, by definition, for almost all the Scope 3 emissions generated by the U.S. economy. Per the GHG Protocol, Scope 3 emissions are a consequence of the activities of a company but occur from sources not owned or controlled by the company (e.g., use of sold energy and refined products by end-market consumers).31 Based on estimates prepared by the nonprofit CDP (formerly the Carbon Disclosure Project) using GHG Protocol reporting standards, approximately 89% of the total emissions from the traditional energy sector are Scope 3 in nature.32 As seen in Figure 4, on a fully loaded basis (i.e., including Scope 1, 2, and 3 emissions), hydrocarbon production accounts for the lion's share of gross U.S. greenhouse gas emissions (82% in 2022) when one factors in downstream fossil fuel combustion, mainly from the electric power and transportation sectors.33

Mandatory company disclosure of Scope 1 and 2 CO2 emissions will also facilitate the calculation of carbon footprints for banks and investment management firms. As with the corporate sector, the only way for financial institutions - 100% of whose attributed greenhouse gas emissions are classified by CDP as Scope 3 in nature34 - to reduce their exposure to transition risk is by decreasing the aggregate emissions profiles of their lending and investment portfolios. If individual portfolio companies in the energy sector and other heavy industry are unwilling or unable to decarbonize, then divestment is the only option for investors.

The unstated but obvious objective of the SEC's climate disclosure rules is to starve fossil fuel companies of the capital needed for business growth, thereby curtailing American oil and gas production. And for all the recent focus on climate and other ESG company resolutions, shareholder votes, proxy fights, and board control during the annual general meeting season, the main defunding of fossil fuels will occur not in the public equity markets but rather in the less transparent credit markets. Bank loans and institutional bonds are the main sources of liquidity for most companies and the cheapest source of capital with which to fund ongoing operations and acquisition-related growth. Ultimately, the disclosure rules will choke off debt capital to certain industries and companies, either by driving up their borrowing costs to prohibitive levels or branding these issuers as basically unworthy of financing at any price.

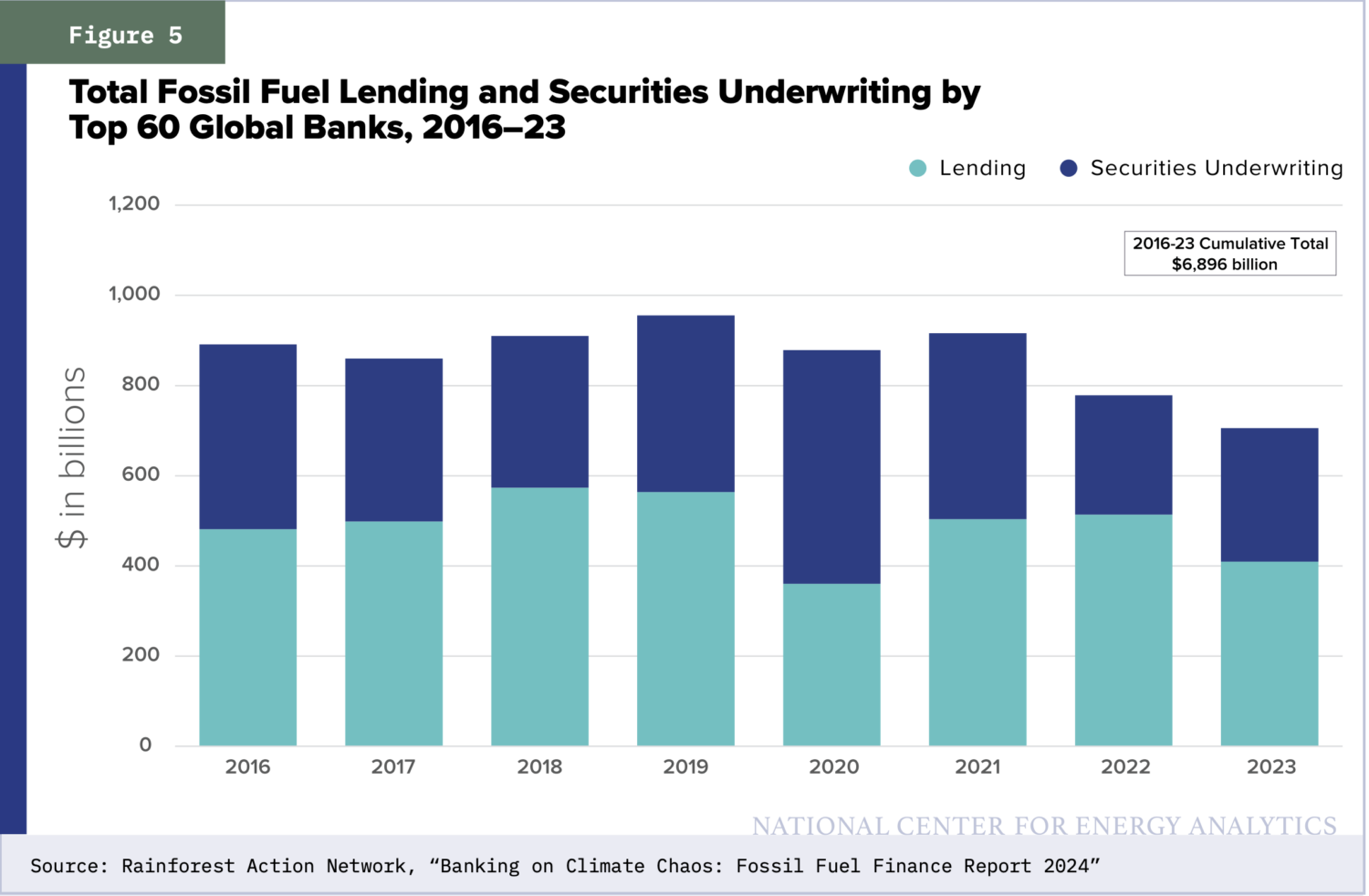

As illustrated in Figure 5, the top 60 global banks provided an aggregate $6.9 trillion of financing - including bank loans and stock and bond underwritings - to fossil fuel companies over 2016-23,35 with much of this bank credit subsequently refinanced through the corporate bond market. Since the 2015 Paris Agreement, sustainable activists have been ramping up public pressure on the world's largest banks to stop financing the traditional energy sector, with several major European banks capitulating in recent years. The SEC's new rules will ensure that this targeted, carbon-based discriminatory policy will now metastasize and work its way into the asset management, insurance company, and pension fund arenas.

The Real Systemic Risk: Decarbonization, Deindustrialization, and Degrowth

Decarbonization - specifically, constraining and eliminating access to and use of hydrocarbons - is the real threat to U.S. financial markets and the American economy. By 2050, the Biden administration's goal is to achieve a net-zero emissions economy.36 On an interim basis, its 2030 objective is to reduce U.S. net greenhouse gas emissions by 50%-52%, versus a 2005 baseline of 6,587 million tonnes of CO2 equivalent, which would imply a target level of approximately 3,228 million tonnes at the midpoint. Such an emissions level has not been seen since the early 1960s, when the American economy was roughly one-fortieth its current nominal size. Notably, this goal would be 41% below the 2022 emissions level of 5,489 million tonnes of CO2 equivalent.37

What will be the macroeconomic impact if the Biden administration succeeds in reducing national emissions as aggressively as planned by 2030? For starters, it will hamstring the U.S. economy while doing nothing to solve the purported problem of global climate change, given that most developing countries - particularly China and India - are not playing by the same climate rules.

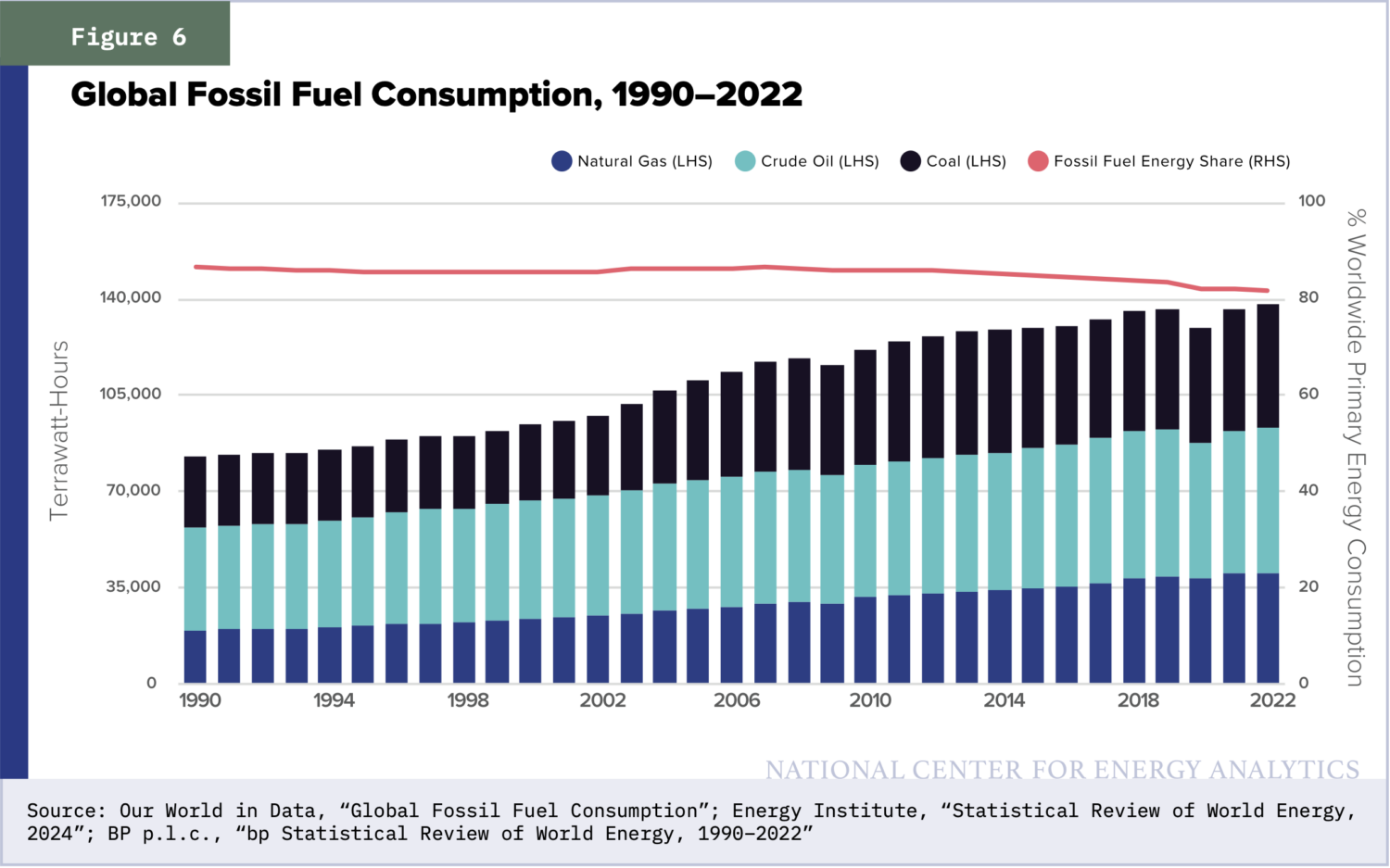

For all the constant noise and attention given to it, there is no global energy transition currently under way. As seen in Figure 6, the world economy continues to be fueled by traditional energy sources. Based on annual data reported by the Energy Institute, roughly 82% of the world's primary energy consumption in 2022 was derived from crude oil, natural gas, and coal, relatively close to 87% in 1990 when the United Nations first started warning the world about the dangers of man-made global warming.38Renewables - excluding hydropower and traditional biomass, the euphemism for wood and manure burning still prevalent in many parts of the Third World - accounted for just under 7% of global primary energy consumption in 2022.39 As a result, annual global greenhouse gas emissions have continued to increase over the past four decades to 57.4 metric gigatons of CO2 equivalent in 2022, more than 50% higher than in 1990, based on emissions data tracked by the United Nations Environment Programme (UNEP).40 In 2022, global emissions were 11% higher than in 2010, which is the baseline for the U.N.'s 2015 Paris Agreement climate target of a 45% reduction by 2030, implying a halving of current 2022 levels over eight years to achieve the Agreement's stated goal to limit the world's average temperature to no more than 1.5oC above preindustrial times.

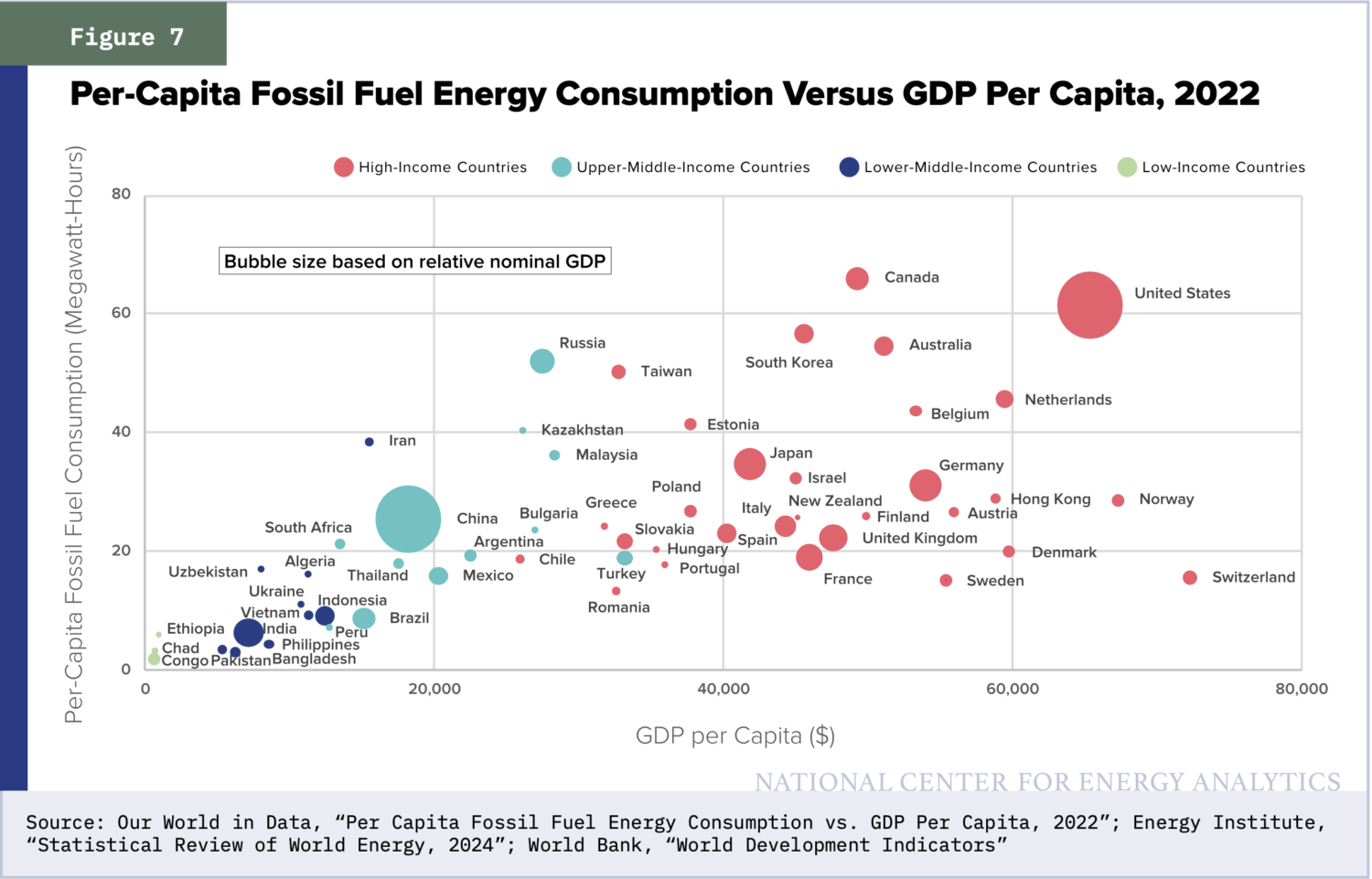

Fossil fuels have been the main driver of industrialization, economic growth, and higher living standards for the past 200 years - a message that has not been lost on the world's poorer emerging market countries. As seen in Figure 7, there is a direct correlation between per-capita fossil fuel consumption and per-capita income levels,41 with most developing countries striving to move up and to the right on this continuum.

The fact that there are no energy-poor, high-income countries demonstrates how energy poverty and economic poverty go hand in hand. The key to building national wealth is increasing, not decreasing, the production and consumption of fossil fuels - and with it, all the attendant hydrocarbon emissions. Not surprisingly, developing economies have constituted the lion's share of the incremental growth in global fossil fuel demand and emissions levels over the past four decades. In fact, since 1990, roughly 67% of the aggregate increase in worldwide fossil fuel primary energy consumption has been driven by the six low-and-middle-income countries commonly referred to as the BRIICS nations: Brazil, Russia, India, Indonesia, China, and South Africa.42 This same BRIICS sovereign grouping accounted for 74% of the total increase in global greenhouse gas emissions over the 1990-2022 period. In 2022, the six BRIICS nations accounted for approximately 47% of worldwide emissions, with China and India alone generating 82% more emissions than the U.S., Canada, U.K., and E.U. combined.43

Thus far, only the U.S. and other wealthy, developed countries in the Northern Hemisphere have been cutting greenhouse gas emissions to align with the policy prescriptions of the U.N., mainly doing so by shutting down coal-fired power plants. Third World governments are not reciprocating, despite lip service paid to the goals of the climate movement. Since the signing of the 2015 Paris Agreement, for every one gigawatt of coal-fired power generation closed in the developed world, nearly three gigawatts of new coal generation capacity have been added by developing countries, mainly in the Asia Pacific region. Based on data tracked by Global Energy Monitor, net coal generation capacity decreased by 136.2 gigawatts in developed countries (largely the U.S. and Europe) post-Paris. During 2016-23, developing countries added a net 390.3 gigawatts of new coal power capacity, with China, India, and Indonesia accounting for 344.3 gigawatts or 88% of this total.44

While many decarbonizing developed countries (including the U.S.) have been able to generate positive real GDP growth while reducing emissions over the past two decades, this has been largely due to the replacement of coal with natural gas as a power generation source. But baseload switching between fossil fuels is no longer kosher, since natural gas is no longer viewed as a bridge fuel by most environmental activists and government regulators.

The negative effects on electricity grids will therefore become more pronounced as wind and solar start to dominate the overall generation mix, especially as power demand ramps up from sources such as AI and data centers. Up until now, some of the pressure placed on grids by growing renewable generation has been masked by flat overall electricity consumption in North America and Europe. This will likely come as a surprise to most Americans, but this is due to the off-shoring of domestic manufacturing to lower-cost developing countries (including China) as part of the globalization push by the business sector over the past 25 years.

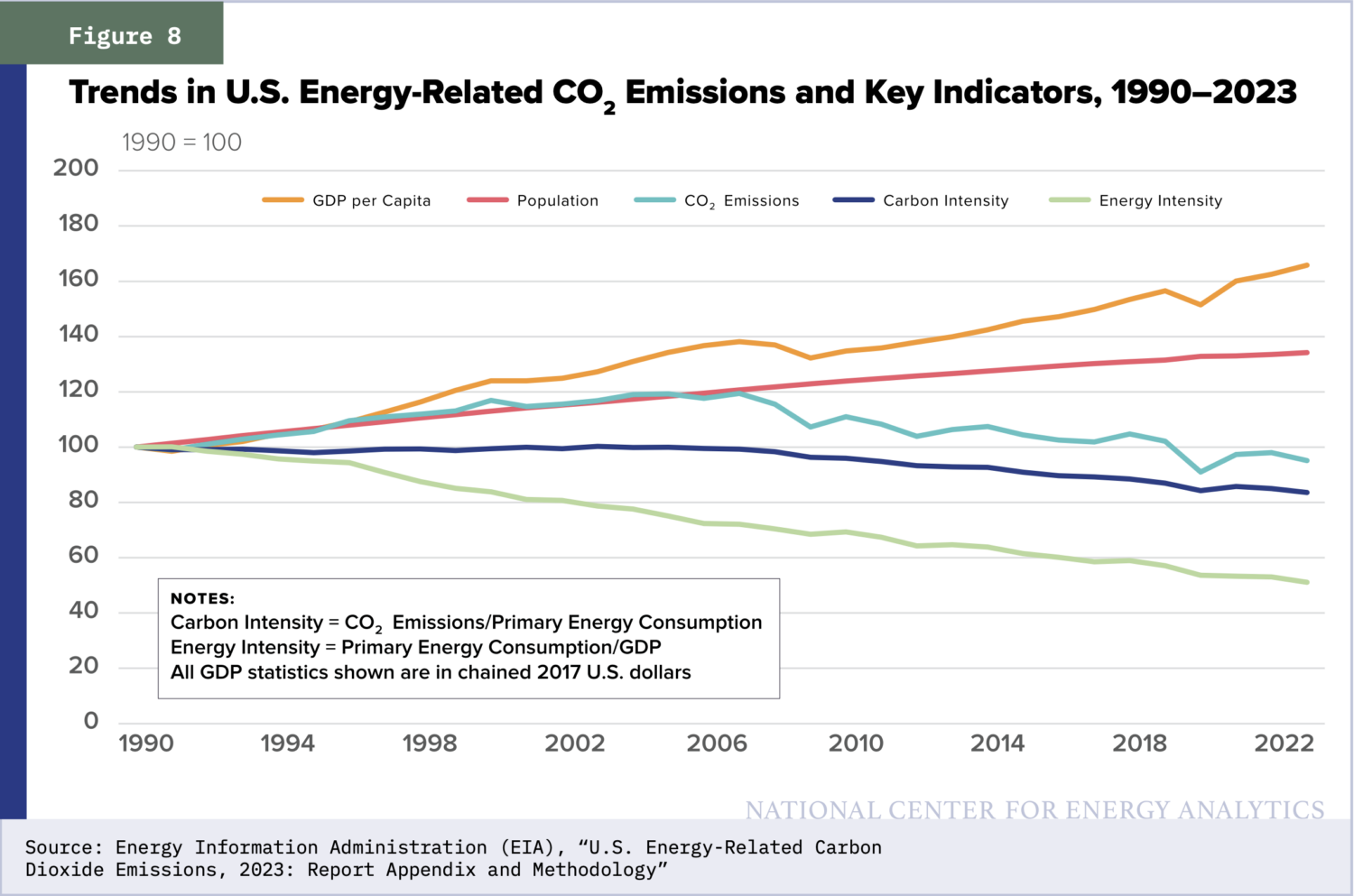

Figure 8 shows the trends in U.S. energy-related CO2 emissions and key economic indicators since 1990.45 Unfortunately, this chart, prepared and touted by the Energy Information Administration (EIA), is highly misleading if one assumes that the U.S. economy can continue to reduce its carbon and energy intensities without jeopardizing GDP per capita.

A major consequence of aggressive decarbonization will be a less reliable American electricity grid, given current EIA projections that wind and solar power will constitute 42% of total net summer capacity and 41% of total U.S. generation by 2030.46 Recent experience shows that an increase in grid instability events is directly correlated with growth in renewable generation capacity. In January 2021, the European continental grid, which relied on wind and solar for roughly 33% of its generation capacity at year-end 2020,47 narrowly avoided a massive blackout when intense cold weather triggered a sharp increase in system-wide electricity demand. California, which had 26% of its generation capacity in intermittent wind and solar at year-end 2021,48 has experienced rolling summer brownouts in recent years during peak periods of demand. In Texas, the statewide Electric Reliability Council of Texas (ERCOT) system experienced a near-total failure during a severe winter storm in February 2021.49 At the time, wind and solar accounted for 29% of total ERCOT generation capacity. That increased to 38% at year-end 2023.50 Ironically, ramping up renewable power will increase the exposure of the U.S. electricity grid to weather-related disruptions or the climate-related physical risks that the SEC is now warning about. In its 2023 Long-Term Reliability Assessment, the North American Electric Reliability Corporation (NERC) noted a high or elevated level of risk of insufficient operating reserves (i.e., power outages) during above-normal conditions in the winter heating or summer cooling seasons for many of the country's regional transmission organizations (RTOs) due to the increasing wind and solar power in the mix.51

The recent growth in interconnections between RTOs as a tool for managing the variability of renewable generation will also spread the risk of potential system failure to larger portions of the country. Depending on the time of year, blackouts and prolonged, widespread power outages will have deadly consequences - as seen in Texas three years ago, when an estimated 246 people died during winter storm Uri due to exposure to the cold.52 On top of increasing mortality rates and risking people's lives to the elements, an unreliable electricity supply system will also disrupt business activity and eventually become a drag on real GDP and income levels.

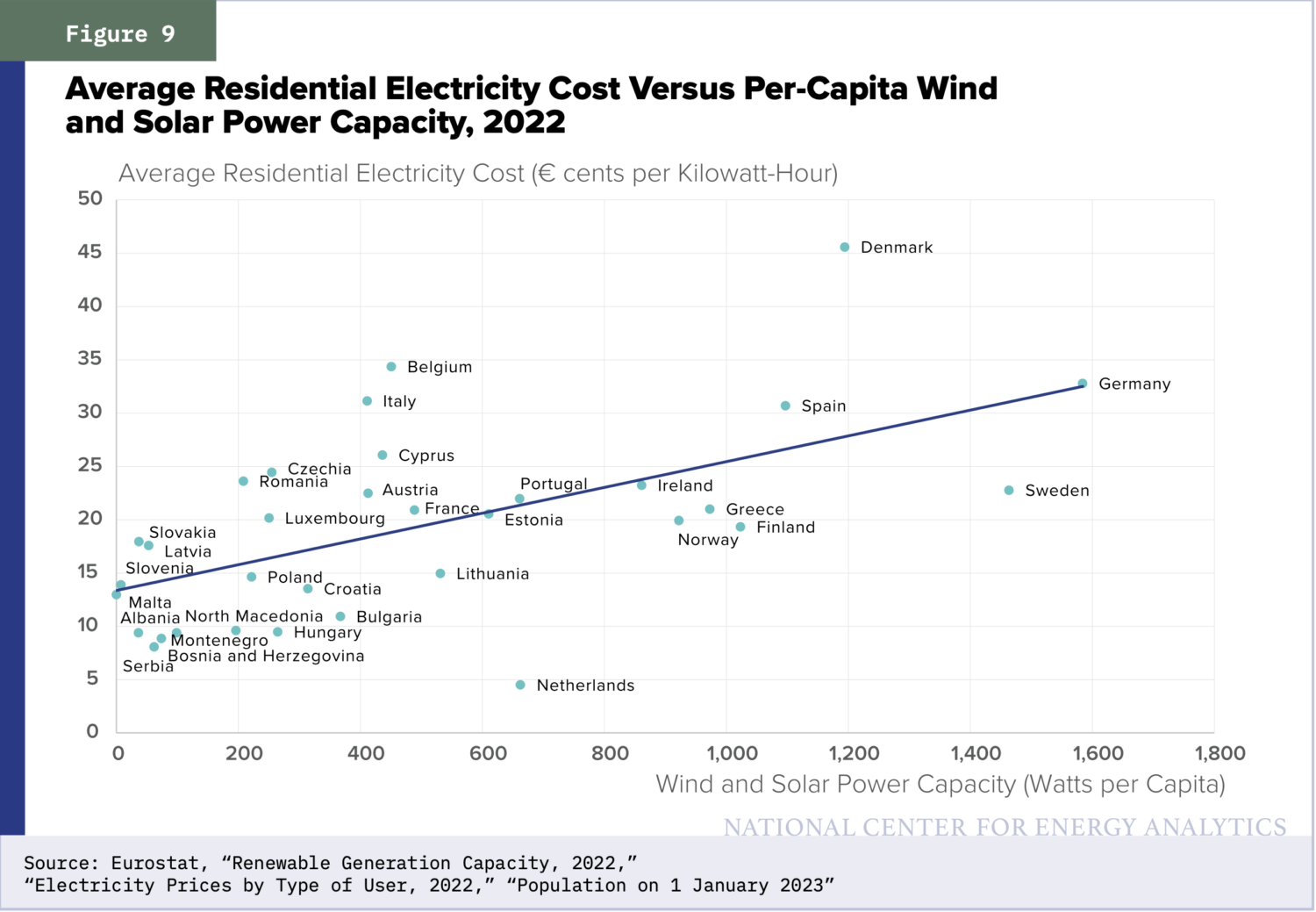

Increased renewable generation will also drive up the average cost of U.S. electricity, since wind and solar power are the most expensive forms of electricity on a levelized cost basis when subsidies are stripped out and backup and storage are added back in.53 Figure 9 shows the correlation between average residential electricity prices and per-capita renewable generation capacity for selected European countries in 2022.54 The highest national electricity prices in the world can now be found in Europe, with Germany standing near the top of the list, with rates nearly three times those in the United States. In the U.S., a similar direct correlation between electricity prices and renewable genera- tion can be seen at the individual state level. Renewable-reliant California currently has the highest retail electricity prices in the lower 48 part of the country (22.33 cents per kWh in 2022), almost double the national average of 12.36 cents per kWh in 2022.55

Apart from electricity prices, constraining the domestic production of fossil fuels - both directly through near-impossible environmental carbon standards and indirectly through financial regulations such as the SEC's climate disclosure rules - will lead to higher oil and gas prices, since the current administration will not be able to crush end-demand sufficiently to prevent a supply-driven price surge. This, in turn, will feed through the entire U.S. economy and raise the cost of almost everything (especially food). Given that hydrocarbons are used to make, transport, or facilitate almost every good or service in the American economy, the ripple effects of a supply-driven increase in oil and gas prices would be pronounced, making the recent non-energy-related jump in U.S. consumer price inflation (+20.3% between January 2021 and July 2024)56 look relatively tame. Hand in hand with higher general price inflation, a regulator-forced shrinking of domestic oil and gas production will lead to significant job losses, given the size of the American energy industry from an employment perspective. Based on data compiled by the Texas Independent Producers and Royalty Owners Association, the U.S. oil and gas industry accounted for a total of 24.1 million direct and indirect jobs in 2023.57

Not maintaining American energy independence by reinvesting in domestic fossil fuel production will shrink the U.S. economy, given PwC estimates that the domestic oil and gas industry contributed 7.6% of U.S. GDP in 2021.58 It will also pose a national security risk by limiting America's ability to project political strength and military might at a critical time in world history. Allowing carbon emissions goals to overrule sound energy policy will place the U.S. at a distinct competitive disadvantage versus China - the world's second-largest economy and America's main commercial rival and geopolitical adversary - which is not bound by the same constrictive climate policies. Electrifying and transitioning the U.S. economy over to clean energy will make the country more dependent on China for everything from electric vehicles to solar panels to critical and rare earth minerals,59 thereby adding to all the China supply- chain vulnerabilities exposed during the COVID-19 pandemic (the majority of which still have not been fixed).

Germany's Failing Economy: A Warning

To gauge the economic risks associated with the pursuit of a low-carbon U.S. future, Germany offers the best decarbonization case study, showing what lies in store if the federal government continues down its current climate policy path. Since embarking on its Climate Action Plan 2050 in 2016, Germany, the largest economy in Europe, has gone from the growth engine of the E.U. bloc to the "sick man of Europe." Climate-driven energy policy has led to a downward spiral of deindustrialization and degrowth. Germany banned oil and gas drilling using hydraulic fracturing (fracking) technology, replaced baseload coal and nuclear power plants with intermittent wind and solar generation, and doubled down on Russian imports for its crude oil, natural gas, and coal needs. Then Russia invaded Ukraine in February 2022, triggering European energy import bans and other economic sanctions.

As Germany's recent experience highlights, a country that does not secure and control its supply of fossil fuel energy - either in-house or through dependable sovereign delivery chains - increases its exposure to global oil and gas price volatility, which can be extreme at times, based on geopolitical developments. When European natural gas prices jumped nearly fivefold in the first eight months of 2022 (hitting a peak of 339.20 / MWh on August 26, 2022),60 due to the war-related shutdown of the Nord Stream natural gas pipeline, German industrial plants and factories - especially those in the automotive and chemicals sector - became instantly uncompetitive and were forced to idle or shut down completely.61 By October 2023, business insolvencies had jumped by 22% year-over-year, followed by a year-over- year increase of 27% during the first quarter of 2024.62

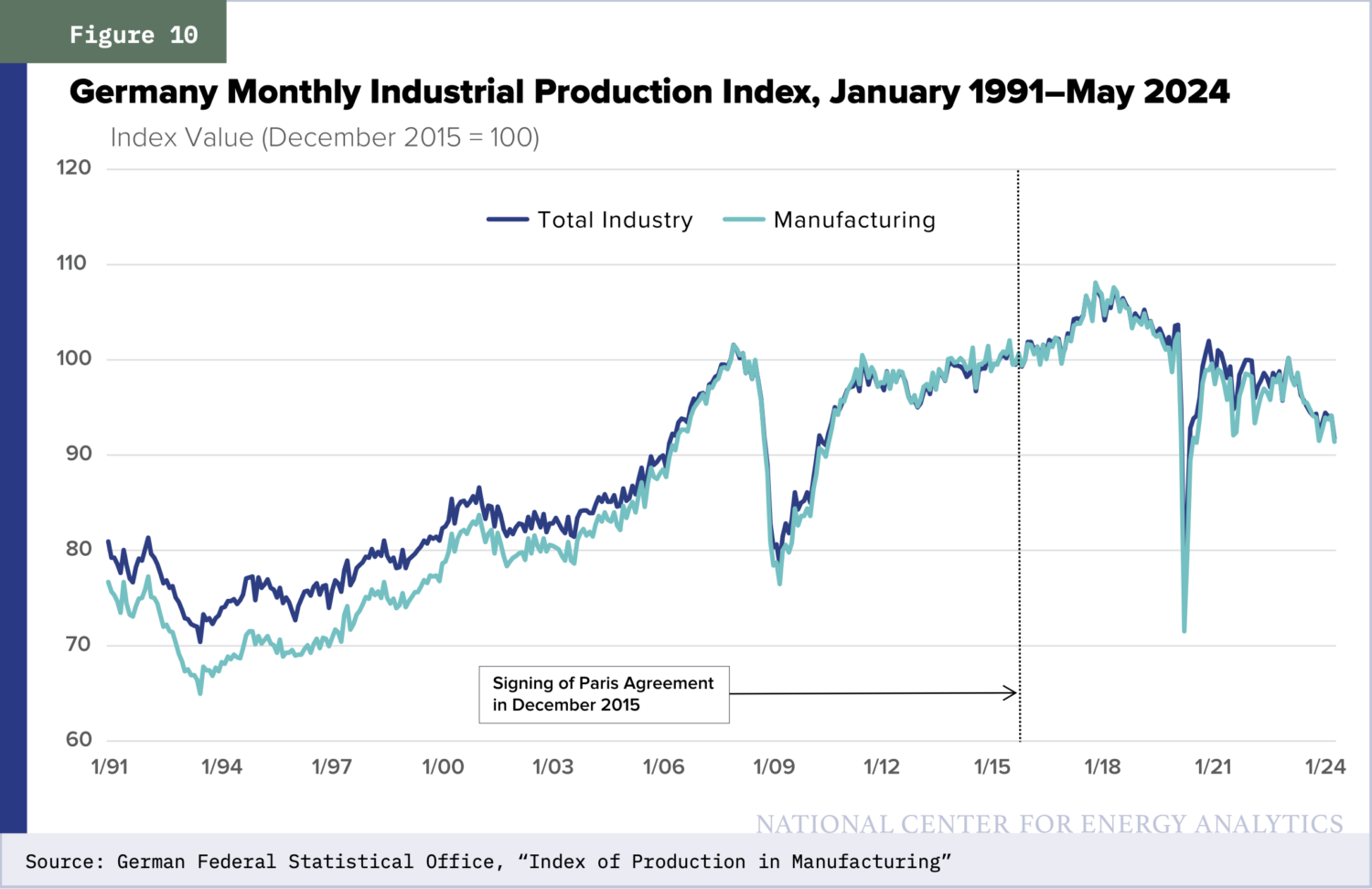

Germany's real GDP growth turned negative in 2023 (-0.3%) after averaging just 1.2% over 2012-22.63 Zero growth (0.1%) is currently forecast for 2024, and Germany's economic stagnation is expected to continue into 2025.64 Even before being whipsawed by natural gas price spikes and power shortages over the 2022-23 period, the German manufacturing sector has been in steady decline for nearly the past decade. As seen in Figure 10, German industrial production (75%-80% manufacturing) peaked in late 2017 and has dropped by nearly 15% since, with no signs of a rebound over the intermediate horizon.65 Nevertheless, Germany is still proceeding with its national plan to completely phase out all remaining coal and nuclear power generation during the current decade.

What has happened in Germany can be this country's fate by the end of the decade - anemic economic growth, higher inflation, increased unemployment levels, and a hollowed out domestic industrial base. It is difficult to see how such a macroeconomic backdrop would be good for the U.S. financial markets. Decarbonized financial markets will be, by definition, more volatile, riskier, and less diversified, with fewer investment choices for investors. By 2030, the U.S. could resemble an emerging financial market more than a developed one.

Since energy-consuming industrial, utility, and technology companies represent the lion's share of most benchmark U.S. stock and bond indexes,66 decarbonization will amplify the market's exposure to fluctuating energy prices. To get an idea of the potential U.S. market impact of volatile energy prices, Germany's DAX Stock Index of 40 leading companies dropped by 25% between January and September 2022 on the back of the above-noted war-related energy price spike.67 Average U.S. corporate credit quality is also likely to trend lower by the end of the decade, dragged down by regulation-driven ratings downgrades for most energy companies as well as other carbon-emitting issuers. In the case of the oil and gas industry, a wholesale re-rating of this large-cap investment-grade sector - potentially down to high-yield territory - cannot be ruled out.

If the SEC's new climate disclosure rules are ultimately implemented, carbon emissions will increasingly set borrowing costs and serve as the gatekeeper for financial market access for energy and other industrial producers. Financial markets will skew away from manufacturing and heavy industry and toward asset-light technology and service companies. Lastly, the ability of the federal government to continue propping up the U.S. financial markets to offset weak underlying economic and corporate fundamentals - as it has basically done since the 2008 global financial crisis - will be severely limited. Easy monetary policy would be constrained by higher structural inflation and loose fiscal policy checked by growing public debt balances ($34.6 trillion, as of the first quarter of 2024, the equivalent of 122% of GDP).68

Concluding Remarks

The SEC's climate disclosure rules - along with the Biden administration's regulatory full court press targeting the fossil fuel industry - have been challenged through the courts. Several lawsuits have been filed since the agency's rules were finalized in March 2024, with the list of plaintiff groups including U.S. states, business groups, trade associations, and individual companies (many of them in the energy sector). In April 2024, the SEC announced that it was voluntarily staying the implementation of its new rules, pending the completion of a consolidated judicial review of nine of these lawsuits by the U.S. Court of Appeals for the Eighth Circuit.69

In objecting to the SEC's climate rulemaking, two main legal arguments have been raised. First, the new rules have been alleged to violate the Administrative Procedure Act by being arbitrary and capricious, since they contradict previous agency policy regarding climate change and were adopted based only on a split 3-2 Commission vote. Second, the rules have been contested on the grounds that they exceed the agency's statutory role as the top cop for the U.S. financial markets.

Issuing climate disclosure rules as a backdoor means of changing the entire U.S. energy mix and restructuring the overall economy would seem to fail the "major questions" test established by the 2022 Supreme Court decision in West Virginia v. Environmental Protection Agency, since this is clearly a policy area of "vast economic and political significance" adopted without explicit congressional - i.e., statutory - authorization. Moreover, the Supreme Court's June 2024 decision in Loper Bright Enterprises v. Raimondo, Secretary of Commerce threw out the precedent of judicial deference to regulatory agency interpretations of the laws they administer that the Supreme Court set 40 years ago in Chevron U.S.A. Inc. v. Natural Resources Defense Council. Loper will bolster these legal arguments.70

The Federal Reserve Board, the Federal Deposit Insurance Corporation, and the Office of the Comptroller of the Currency within the Treasury Department have issued similar climate-related agency guidance. This raises an interesting issue: Should the U.S. Congress consider taking affirmative legislative action to restrain the SEC and all U.S. financial regulators from crossing over into energy and economic policy by using the pretext that climate change represents financial risk?

The SEC's stated mission is to "protect investors, maintain fair, orderly, and efficient markets, and promote capital formation." None of these boxes is ticked with the new climate disclosure rules. Investors do not need to be protected by the SEC from climate - actually, weather - change. Other than a small but vocal minority of ESG-focused investors, most Wall Street institutional and retail investors do not view climate change as an investment or financial risk. Up until now, climate - and every other nonfinancial ESG factor, for that matter - has had no impact on financial asset prices, so investors are not being hurt by inflated asset prices or greenwashing fraud. By ignoring the market's clear disregard for climate change as a fundamental factor or relative value driver, the SEC is betraying its lack of faith in market efficiency.

Moreover, rather than reducing market risk by mandating disclosure about climate-related physical and transition risks and carbon emissions profiles, the new SEC rules will increase the macroeconomic and financial risks for the United States. Decarbonizing the financial markets by defunding the oil and gas sector is the real systemic risk that the SEC should be focusing on. In this regard, the SEC appears to have violated long-standing guidance on the economic impact analysis that the agency must prepare for all new rulemaking.

In its cost-benefit review for its new climate rules, the SEC mainly focused on the micro effects and the direct compliance costs for individual companies, which it estimated in an average annual range of $197,000-$739,000 over the first 10 years of reporting, depending on the nature of a registrant's business and the magnitude of its carbon emissions.71 In the agency's mind, such incremental issuer expense is more than offset by the qualitative informational and other benefits of the disclosures to investors. What the SEC ignored was how its new rules would affect the macroeconomy by changing investor behavior, redirecting capital flows, and catalyzing the other anti-fossil fuel regulations promulgated by the federal government. Yet under the Administrative Procedure Act, the SEC has a "statutory obligation to determine as best it can the economic implications" of all its rules, which clearly was not done in this case.72

Most egregiously, with these climate disclosure rules, the SEC will no longer be an objective market referee, at least when it comes to the ESG factor of climate change. Despite its claims that its intent is "not to address climate-related issues more generally," the SEC will now become an active partisan player in the Biden administration's drive to decarbonize the U.S. economy, in direct contravention of its regulatory mandate to remain impartial and simply ensure full disclosure and fair dealing across well-functioning financial markets. By mandating the integration of climate factors into both corporate policy and investment risk management, the Commission will be supplanting the business role of corporate executives, bank credit officers, and investment portfolio managers, thereby crossing an important governance line.

Appendix: The Federal Full Court Press

Over the fiscal years 2016-22, the federal government funneled roughly $90 billion of energy subsidies (mainly tax credits) toward the construction of new solar and wind power generation, biodiesel production, and the consumer purchase of electric vehicles.73 Such transition spending was taken to a whole new level in August 2022, with the passage of the Inflation Reduction Act (IRA), which included a headline $369 billion of climate-related expenditures.74 Despite such government largess, wind and solar power accounted for only 17.1% of total U.S. electricity generation in 2023, according to the Energy Informa- tion Administration (EIA).75 Based on data reported by the U.S. Department of Agriculture, aggregate biodiesel and renewable diesel production in 2023 equated to just 7.1% of total distillate fuel sales that year.76 EVs constituted only 7.6% of U.S. new vehicle sales in 2023, according to Kelley Blue Book.77

At the same time, the federal government has supplemented subsidies and grants with policies aimed at crippling domestic fossil fuel demand and supply. Using a "whole-of-government" approach, the list is long, but includes the following:

- In March 2024, the Environmental Protection Agency (EPA) finalized new carbon-focused, fleet-based emissions standards for passenger cars and light trucks, which require that an ever-in- creasing percentage of new vehicles sold in the U.S. must be zero-emission rather than gas-powered. Beginning with the 2027 model year, internal combustion engine (ICE) vehicle sales are capped at 64% of total U.S. sales, dropping down to 29% by 2032.78

- In April 2024, the EPA passed new rules for reducing carbon emissions from fossil fuel-fired power plants. By 2032, all operating coal plants and any new natural gas plants will be required to have carbon capture and sequestration (CCS) systems installed in order to capture 90% of their carbon emissions.79 Since CCS technology does not currently exist at an economic scale to justify such capital spending,80 this will necessarily shut down all remaining baseload coal facilities and put a halt to all new natural gas plant construction. On the supply side, President Biden issued a moratorium on all federal oil and gas leasing activity immediately upon taking office in 2021.81 Over the past three years, the Bureau of Land Management (BLM) within the Department of the Interior (DOI) has conducted lease sales only under court order. The BLM's 2024-29 offshore drilling plan calls for only three Gulf of Mexico auctions, the bare minimum and smallest leasing program in U.S. history, more than 80% below the average for the previous five BLM leasing programs, dating back to 1992.82

- In 2023, the EPA passed a methane tax - the first carbon (equivalent) tax to be implemented in the U.S. - that fines fugitive industry emissions at a punitive rate starting at $900/tonne in 2024, rising to $1,500/tonne by 2026.83 Embedded in the new regulation is a phased-in ban on the flaring of associated natural gas from new oil wells, which, in the absence of new natural gas pipelines, would shut in new oil production.

- In November 2022, the U.S. Fish & Wildlife Service (USFWS) constrained development drilling in the most prolific oil-pro- ducing basin in the country. It did so by adding the southern lesser prairie-chicken to its endangered species list,84 followed by the addition of the dunes sagebrush lizard in May 2024.85 Both species are indigenous to the Permian Basin, straddling West Texas and New Mexico, which is the nation's premier oil- and gas-producing region.

- The EPA continues to evaluate whether to redesignate the Permian Basin as an ozone non-attainment zone.86 If put into effect, that would further restrict oil and gas production in the region by requiring air permits before constructing new oil and gas facilities or modifying existing energy infrastructure in the region's affected counties.

- In January 2024, the Department of Energy (DOE) announced a pause on liquefied natural gas (LNG) export permit approvals to non-Free Trade Agreement countries,87 which, as a group, account for almost all current U.S. LNG exports. Since LNG exports are now the marginal driver of U.S. natural gas demand - they totaled 11.9 billion cubic feet per day in 2023, equating to 11.5% of total supply and making America the leading LNG exporter in the world - such a ban would cap domestic production levels going forward.

- In April 2024, the DOI, working through the BLM, finalized a new Public Lands Rule,88 which prioritizes conservation over resource development in the management of all public lands, and a companion Fluid Mineral Leases and Leasing Process Rule,89 which raises the bonding costs and royalty rates for oil and gas exploration and production companies while simultaneously limiting all oil and gas leasing on onshore public lands to areas with existing infrastructure. This latter provision will limit industry reserve growth through the drill-bit and the natural de-risking of prospective resource plays - what the DOI dismissively refers to as "speculation."

- In 2022, the country's Strategic Petroleum Reserve (SPR), which was created to provide a buffer against geopolitical and weather disruptions to crude oil supply, was drained for political reasons (i.e., to temper rising gasoline prices). Currently filled to just 53% of capacity, the SPR now stands at stock levels not seen since the early 1980s, with no credible plans to replenish it in sight.90 The long-awaited court-mandated environmental ruling on the Dakota Access Pipeline (DAPL) has been dragged out for more than three years by the Army Corps of Engineers and the Department of Justice,91 even though the oil pipeline poses no environmental risk where it crosses the Missouri River. Shutting in existing energy infrastructure like DAPL by revoking a legally issued environmental permit would set a dangerous new precedent for stranding U.S. oil and gas assets.

Viewed in this context, the SEC's climate disclosure rules are just part of a coordinated climate plan by the current administration and the latest in a series of regulatory attacks against the oil and gas industry. The transition risk component of the new SEC rules is meant to discourage investment in the traditional energy sector by highlighting the outsize regulatory, litigation, contingent liability, and reputational risks now facing the industry due to government climate policies. Notably, the SEC rules will further heighten these risks by providing more ammunition for litigious ESG activists looking to sue energy companies, given that the new climate disclosures will be subject to potential liability under both the 1933 and the 1934 Acts.92

Interested in learning more?

Tice's NCEA blog post: SEC's Climate Disclosure Rules: A Threat to Economic Growth and Energy Security.

Read the Press Release.

Watch the Interview:

https://youtu.be/GG4ojL24nDo

Endnotes

- Thomas Catenacci, "JPMorgan, BlackRock Drop Out of Massive UN Climate Alliance in Stunning Move,"

- European Commission (EC), "Corporate Sustainability Reporting," accessed July 10, 2024.

- "Sustainability-Related Disclosure in the Financial Services Sector," accessed July 10, 2024.

- EC, "A European Green Deal: Striving to Be the First Climate-Neutral Continent," accessed July 10, 2024.

- EC, "EU Taxonomy for Sustainable Activities," accessed July 10, 2024.

- Financial Conduct Authority, "Sustainability Disclosure Requirements (SDR) and Investment Labels," November 2023.

- U.S. Securities and Exchange Commission (SEC), "Final Rules: The Enhancement and Standardization of Climate-Related Disclosures for Investors," Mar. 6, 2024. (hereafter "Final Rules.")

- SEC, "SEC Announces Enforcement Task Force Focused on Climate and ESG Issues," Mar. 4, 2021.

- SEC, "Final Rules," 12.

- Myanna Lahsen and Jesse Ribot, "Politics of Attributing Extreme Events and Disasters to Climate Change," Wiley Interdisciplinary Reviews: Climate Change, Dec. 8, 2021.

- SEC, "Final Rules," 20, 67, 89, 92, 459.

- S&P Dow Jones Indices, "Fact Sheet for S&P 500 Index, July 31, 2024," accessed Aug. 16, 2024.

- Our World in Data, "Economic Damages from Disasters as a Share of GDP, United States, 1960 to 2022," accessed July 10, 2024. Underlying chart data sourced from UCLouvain and World Bank. Supplementary data sourced from the Insurance Information Institute, National Oceanic and Atmospheric Administration, and U.S. Bureau of Economic Analysis.

- Yahoo!Finance, "Price Chart for S&P 500 Index, 9/30/05 to 3/31/06," accessed July 10, 2024.

- Yahoo!Finance, "Price Chart for S&P 500 Energy Index, 9/30/05 to 3/31/06," accessed July 10, 2024.

- Securities Industry and Financial Markets Association (SIFMA), "Research Report: Corporate Bond Market," Research Quarterly 111, no. 6 (May 2008): 10.

- John Butters, "Earnings Insight," FactSet, Aug. 16, 2024.

- Financial data sourced from annual SEC 10-K filings of Cheniere Energy, Inc.

- Data compiled from National Association of Insurance Commissioners, "U.S. Property & Casualty and Title Insurance Industries: 2016-2023 Full Year Results," and Insurance Information Institute, "Facts + Statistics: U.S. Catastrophes."

- Aon plc, "Reinsurance Market Dynamics," April 2024.

- National Association of Insurance Commissioners, "U.S. Property & Casualty and Title Insurance Industries: 2023 Full Year Results," accessed July 10, 2024.

- Risk & Insurance, "P&C Insurers Faced Rising Downgrades, Higher Costs in 2023," Mar. 12, 2024.

- S&P Dow Jones Indices, "Fact Sheet for S&P 500 Index, July 31, 2024," accessed Aug. 16, 2024.

- S&P Dow Jones Indices, "S&P Market Attributes Web File, July 31, 2024," accessed Aug. 16, 2024.

- Council on Foreign Relations, "Onshoring Semiconductor Production: National Security Versus Economic Efficiency," Apr. 17, 2024, accessed July 10, 2024

- SEC, "Final Rules," 243.

- SEC, "Final Rules," 92-93.

- SEC, "Final Rules," 679.

- GHG Protocol, "Corporate Standard," accessed July 10, 2024.

- Environmental Protection Agency (EPA), "Greenhouse Gas Inventory Data Explorer," accessed July 10, 2024.

- GHG Protocol, "Corporate Standard," accessed July 10, 2024.

- Carbon Disclosure Project (CDP), "CDP Technical Note: Relevance of Scope 3 Categories by Sector."

- EPA, "Greenhouse Gas Inventory Data Explorer," accessed July 10, 2024.

- CDP, "CDP Technical Note: Relevance of Scope 3 Categories by Sector."

- Rainforest Action Network, "Banking on Climate Chaos: Fossil Fuel Finance Report 2024."

- The White House, "FACT SHEET: President Biden Sets 2030 Greenhouse Gas Pollution Reduction Target Aimed at Creating Good-Paying Union Jobs and Securing U.S. Leadership on Clean Energy Technologies," Apr. 22, 2021.

- Ibid.

- Our World in Data, "Global Fossil Fuel Consumption," accessed July 10, 2024. Underlying chart data sourced from Energy Institute and BP p.l.c.

- Energy Institute, "Statistical Review of World Energy, 2024."

- United Nations Environment Programme (UNEP), "Emissions Gap Report 2023: Broken Record."

- Our World in Data, "Per Capita Fossil Fuel Energy Consumption vs. GDP Per Capita, 2022," accessed July 10, 2024.

- Figure calculated from data sourced from Energy Institute and BP p.l.c.

- EC, "JRC Science for Policy Report: GHG Emissions of All World Countries 2023," accessed July 10, 2024.

- Global Energy Monitor, "Global Coal Plant Tracker," accessed July 10, 2024.

- Energy Information Administration (EIA), "U.S. Energy-Related Carbon Dioxide Emissions, 2023: Report Appendix and Methodology," April 2024.

- EIA, "Annual Energy Outlook 2023," Table 8. Electricity Supply, Disposition, Prices, and Emissions; Table 9. Electricity Generating Capacity; Table 16. Renewable Energy Generating Capacity and Generation," Mar. 16, 2023, accessed July 10, 2024.

- Eurostat, "Maximum Electrical Capacity, EU, 2000-2021 (MW)," July 7, 2023, accessed July 10, 2024.

- California Energy Commission, "Electric Generation Capacity and Energy," accessed July 10, 2024.

- Dominique Finon, "Intermittent Renewables and the Threat of Blackouts, How to Deal with It?" Encyclopedie de l'energie, Oct. 12, 2022.

- Electric Reliability Council of Texas (ERCOT), "Fact Sheets," November 2021, August 2024.

- North American Electric Reliability Corporation (NERC), "2023 Long-Term Reliability Assessment," December 2023.

- Patrick Svitek, "Texas Puts Final Estimate of Winter Storm Death Toll at 246," Texas Tribune, Jan. 2, 2022.

- Lazard, "LCOE+ Report," April 2023.

- All underlying chart data for electricity prices, renewable generation capacity, and population sourced from Eurostat.

- EIA, "US Electricity Profile 2022," accessed July 10, 2024.

- U.S. Bureau of Labor Statistics, "CPI Inflation Calculator," accessed July 10, 2024

- Texas Independent Producers and Royalty Owners Association, "2024 State of Energy Report," Mar. 21, 2024, accessed July 10, 2024.

- PwC, "Impacts of the Oil and Natural Gas Industry on the US Economy in 2021," April 2023.

- Teresa Mull, "The US Is Greening Itself Toward More Dependence on China," The Spectator, Apr. 7, 2023

- Yahoo!Finance, "Price Chart for Dutch TTF Natural Gas Calendar, 12/31/21 to 9/29/22," accessed July 10, 2024.

- Anna Cooban, "Rocketing Energy Costs Are Savaging German Industry," CNN Business, Oct. 7, 2022.

- Richard Connor, "Germany Sees Company Bankruptcies Soar," Deutsche Welle, June 14, 2024.

- German Federal Statistical Office, "Gross Domestic Product Down 0.3% in 2023," Jan. 15, 2024.

- EC, "Economic Forecast for Germany," May 15, 2024, accessed July 10, 2024.

- German Federal Statistical Office, "Index of Production in Manufacturing," accessed July 10, 2024.

- As of June 28, 2024, the energy, industrials, utilities, materials, real estate, and information technology sectors constituted an aggregate 50.8% of the S&P 500 Index. As of July 11, 2024, the energy, capital goods, basic industry, electric, REIT, technology, and communications sectors together accounted for 40.9% of the iShares Broad USD Investment Grade Corporate Bond ETF.

- Yahoo!Finance, "Price Chart for DAX Performance Index, 1/3/22 to 9/29/22," accessed July 10, 2024.

- Federal Reserve Bank of St. Louis, Economic Research, "Federal Debt: Total Public Debt," accessed July 10, 2024.

- DLA Piper, "SEC Stays Climate Rules: An Overview of Ongoing Legal Challenges," Apr. 9, 2024, accessed July 10, 2024.

- DLA Piper, "Chevron Overruled: In Loper Bright v. Raimondo, the Supreme Court Reshapes the Regulatory Landscape," June 28, 2024, accessed July 10, 2024.

- SEC, "Final Rules," 740.

- SEC, "Current Guidance on Economic Analysis in SEC Rulemakings," Mar. 16, 2012.

- U.S. Energy Information Administration (EIA), "Federal Financial Interventions and Subsidies in Energy in Fiscal Years 2016-2022," August 2023, accessed July 10, 2024.

- Earthjustice, "What the Inflation Reduction Act Means for Climate," Aug. 16, 2022, accessed July 10, 2024.

- EIA, "Electric Power Monthly, Table 1.1. Net Generation by Energy Source: Total (All Sectors), 2014-May 2024," accessed July 10, 2024.

- U.S. Department of Agriculture, "U.S. Bioenergy Statistics," accessed July 10, 2024. Distillate fuel sales denominator sourced from EIA, "U.S. Product Supplied of Distillate Fuel Oil."

- Kelley Blue Book, "Americans Buy Nearly 1.2 Million Electric Vehicles to Hit Record in 2023, According to Latest Kelley Blue Book Data," Jan. 16, 2024, accessed July 10, 2024.

- U.S. Environmental Protection Agency (EPA), "Final Rule: Multi-Pollutant Emissions Standards for Model Years 2027 and Later Light-Duty and Medium-Duty Vehicles," Mar. 20, 2024.

- EPA, "Final Rule: New Source Performance Standards for Greenhouse Gas Emissions from New, Modified, and Reconstructed Fossil Fuel-Fired Electric Generating Units; Emission Guidelines for Greenhouse Gas Emissions from Existing Fossil Fuel-Fired Electric Generating Units; and Repeal of the Affordable Clean Energy Rule," Apr. 25, 2024.

- Julia Attwood, "US Coal Plants Face New Rule: Capture CO2 or Shutter," BloombergNEF, May 2, 2024.

- Matthew Brown, "Biden Halts Oil and Gas Leases, Permits on US Land and Water," Associated Press, Jan. 21, 2021.

- Zack Budryk, "Biden Administration Issues Final Five-Year Offshore Drilling Plan," The Hill, Dec. 15, 2023.

- EPA, "Standards of Performance for New, Reconstructed, and Modified Sources and Emissions Guidelines for Existing Sources: Oil and Natural Gas Sector Climate Review," Dec. 2, 2023.

- U.S. Fish & Wildlife Service (USFWS), "Lesser Prairie Chicken Listed Under the Endangered Species Act," Nov. 17, 2022.

- USFWS, "The Service Lists Dunes Sagebrush Lizard," May 17, 2024, accessed July 10, 2024.

- Andreas Exarheas, "EPA Clarifies Permian Redesignation Position," Rigzone, Jan. 10, 2023.

- U.S. Department of Energy (DOE), "DOE to Update Public Interest Analysis to Enhance National Security, Achieve Clean Energy Goals and Continue Support for Global Allies," Jan. 26, 2024, accessed July 10, 2024.

- U.S. Bureau of Land Management (BLM), "Biden-Harris Administration Finalizes Strategy to Guide Balanced Management, Conservation of Public Lands," Apr. 18, 2024, accessed July 10, 2024.

- BLM, "BLM Ensures Fair Taxpayer Return, Strengthens Accountability for Oil and Gas Operations on Public Lands," Apr. 12, 2024, accessed July 10, 2024.

- Cathy Landry, "US Energy Department Stops Crude Purchases to Refill Strategic Oil Stockpile," Oil & Gas Journal, Apr. 5, 2024.

- Michael Anthony, "Environmental Impact Statement on DAPL 'On the Shelf,' Could Be Released Around Election Day," KFYR TV, Mar. 15, 2024.

- U.S. Securities and Exchange Commission (SEC), "Final Rules: The Enhancement and Standardization of Climate-Related Disclosures for Investors," Mar. 6, 2024, 583.

Continue Reading

Unreasoned Decisionmaking: FERC's Ever-Changing Methodology for Estimating the Return On Equity

The financial crisis that began in 2008 led to unprecedented actions by the U.S. Federal Reserve (Fed) to lower interest rates and stimulate the economy.