The Coal Reality That Western Policy Ignores

-6%20(8).png)

One outcome from the disruption in oil and gas markets caused by the war against Iran has been a renewed appreciation...

Listen

The Issue

One outcome from the disruption in oil and gas markets caused by the war against Iran has been a renewed appreciation for the foundational importance of coal in meeting global energy demand. As Asia was forced to reduce its reliance on liquid natural gas (LNG) following the closure of the Strait of Hormuz, thermal coal markets responded. Bangladesh, Japan, the Philippines, South Korea, Taiwan, Vietnam, and others—all capable of shifting from LNG to coal for reliable power generation—recorded an increase in coal imports.1 Europe, too, increased coal use to bolster energy security.2

Even prior to the war, global coal demand had reached record levels of about 9 billion metric tons in 2025, with thermal coal trade measured at well over 1 billion metric tons (Bt) annually.3

Figure 1: There Is No Transition, Only Addition

.png)

* Other includes geothermal, biomass, and other sources of renewable energy such as biofuels.

Sources: Adapted from Lars Schernikau, “Coal Keeps the Lights On . . . Are We Experiencing a ‘New’ Renaissance of Coal?,” The Unpopular Truth (blog), March 18, 2026. Data from Energy Institute, 2025 Statistical Review of World Energy, 74th ed. (Energy Institute, 2025); and “Electricity Data Explorer,” Ember, accessed June 22, 2026, https://ember-energy.org/data/electricity-data-explorer.

Despite coal’s persistent rise in global energy supply—accounting for over one-third of all electricity generation (see figure 1)—Western energy policies continue to assume its structural decline, seeking to marginalize its role through regulation and financing constraints. Markets, however, treat coal as a critical fuel and essential industrial input. In 2024, a report by the Association of Southeast Asian Nations (ASEAN) Centre for Energy declared that “coal currently outperforms other energy sources in terms of supply security, reliability, affordability and—to some extent—sustainability in ASEAN’s power generation,” while adding that any “strategic shift from coal should be implemented at the right time as soon as economic and environmentally friendly alternatives at the grid scale become available.”4

Given its cost competitiveness and wide availability, markets indicate that coal will not be possible to replace in the foreseeable future, especially (but not only) for critical industrial applications. Last year, the International Energy Agency (IEA) forecast—under its Net Zero Emissions by 2050 Scenario—a decline in coal demand of about 35% by 2035.5

In May 2026, the IEA acknowledged that “coal remains critical to meet growing electricity demand and fulfil key power system needs” but continued advocating for rapid phaseouts, even in Southeast Asia.6 Yet the data indicate sustained or growing reliance on coal in emerging markets, and persistent global instability suggests that the same might hold true for the developed world—for decades to come. Those seeking a lower-coal future may need to recognize the counterintuitive value of targeted investment in coal to prevent power disruptions, higher costs, and unintended environmental or reliability consequences.

The Reality

Electricity, industry, trade, fertilizer production, and energy security all depend on coal to varying degrees. Coal serves as the most important fuel and chemical reductant for producing key materials of modern civilization, central to supply chains for steel, cement, metals, fertilizers, consumer goods, electronics, and energy infrastructure itself. Like oil and gas, coal is the material basis for thousands of everyday products beyond its utility as an energy source.

When Western countries offshored heavy industry, production shifted to regions where coal remains dominant. Global coal consumption has risen from just over 6 Bt in 2008 to almost 9 Bt in 2025 (see figure 2).7 Seaborne coal trade (thermal and metallurgical) grew from about 800 million metric tons (Mt) to roughly 1.5 Bt in the same time frame, making it one of the world’s largest material flows. Coal accounts for almost 10% of all globally extracted mineral resources.8 Meanwhile, air quality has improved significantly worldwide.9

Figure 2: Global Coal Production

Note: Totals exceed 9 Bt. Bt denotes billion metric tons, and Mt denotes million metric tons.

Sources: Adapted from Lars Schernikau, “Coal Keeps the Lights On . . . Are We Experiencing a ‘New’ Renaissance of Coal?,” The Unpopular Truth (blog), March 18, 2026. Data from International Energy Agency (IEA), “Demand,” in Coal 2025—Analysis and Forecast to 2030 (IEA, 2025), 12–42; and Schernikau’s independent research and analysis.

Asia has driven this growth. In 2025 alone, China commissioned about 80 GW of new coal-fired capacity—equivalent to roughly 70% of Europe’s remaining coal fleet.10 China’s coal capacity is likely to continue expanding for grid stability, even as utilization rates adjust downward due to increases in wind and solar power.11 India, too, plans substantial increases, with coal consumption projected to rise from about 1.2 Bt today to roughly 2.6 Bt by 2047 and about 100 GW of new coal plants planned within the next decade.12

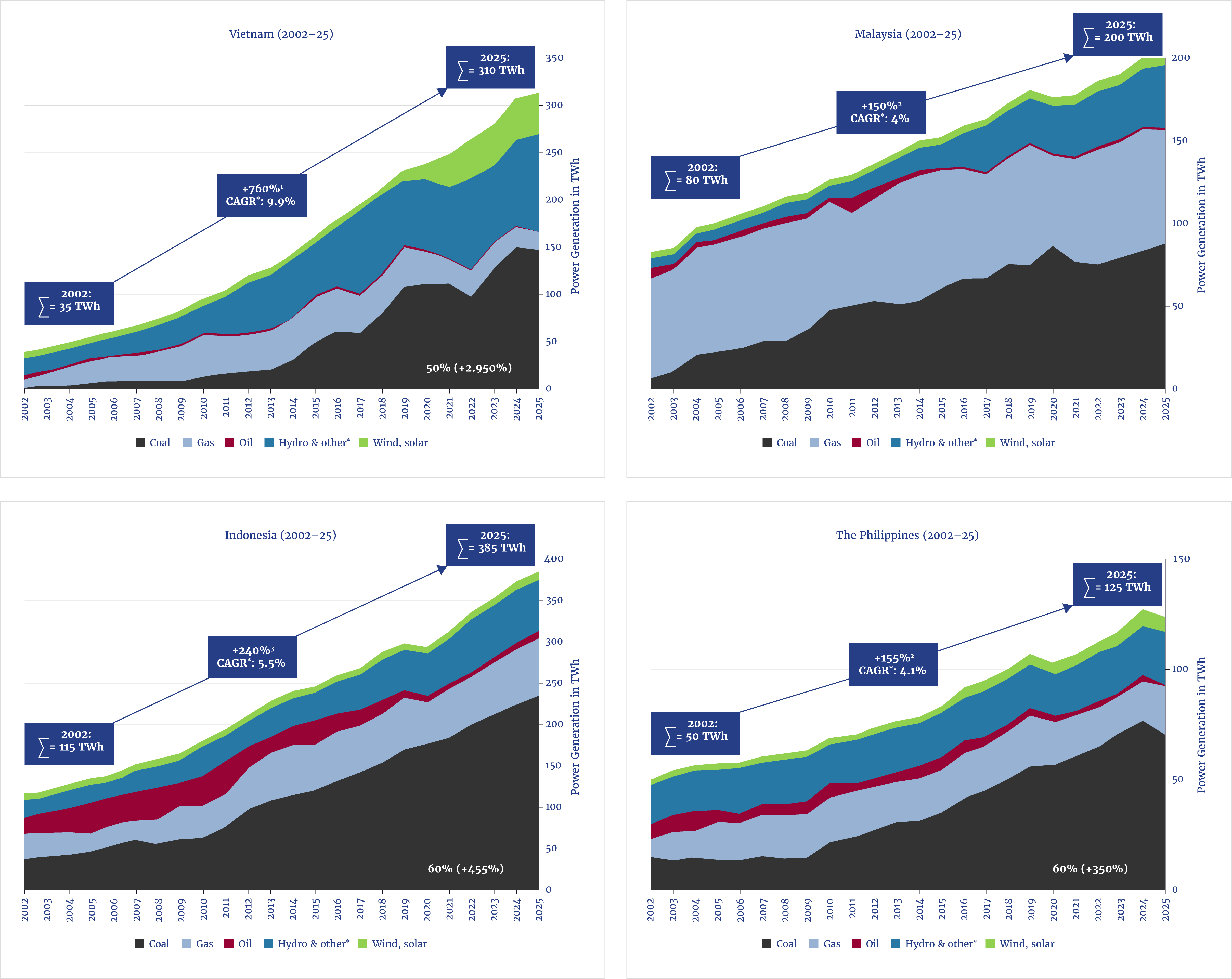

Other Asian countries have seen dramatic growth (see figure 3). Vietnam’s coal consumption has increased 750% in the last two decades. Malaysia, Indonesia, and the Philippines have more than doubled or tripled their consumption since the beginning of the millennium. All told, coal-fired thermal plants produce over one-third of the world’s electricity.

Figure 3: Electricity Generation in Select Southeast Asian Countries

* Other includes geothermal, biomass, and other sources of renewable energy such as biofuels.

Sources: Adapted from Schernikau, “Coal Keeps the Lights On . . . Are We Experiencing a ‘New’ Renaissance of Coal?,” The Unpopular Truth (blog), March 18, 2026. Data from “Electricity Data Explorer,” Ember, accessed June 25, 2026, https://ember-energy.org/data/electricity-data-explorer.

Keeping Lights On and Powering Industry

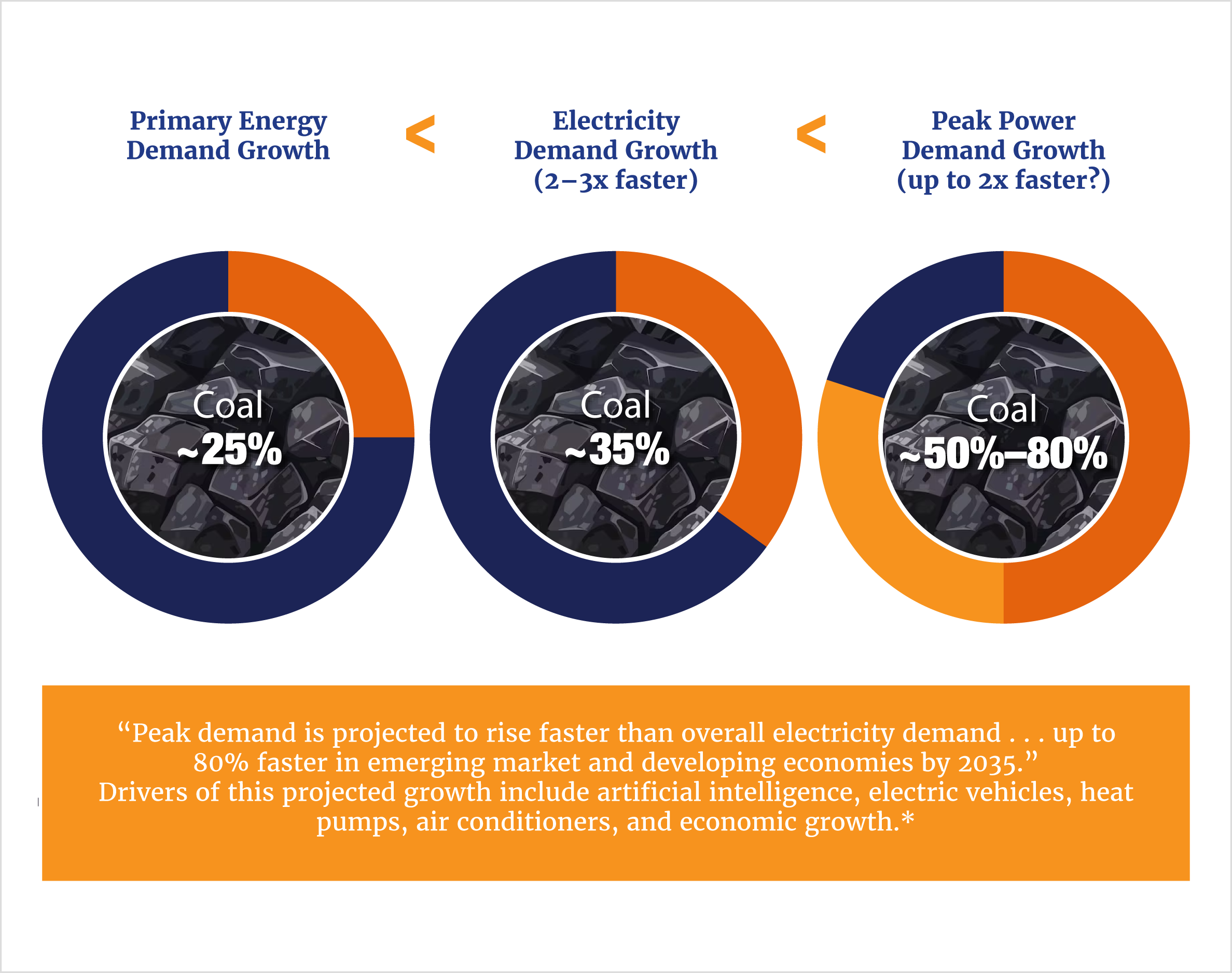

Energy systems operate in three interconnected tiers: primary energy, electricity, and peak power demand (see figure 4). While all have grown alongside population and economic development, electricity demand has outpaced primary energy growth. Peak demand has grown fastest—in some regions, twice as fast as electricity. Coal dominates the energy sources capable of meeting both baseload and peak power demand and, perhaps surprisingly, is most critical in meeting peak power demand. Coal’s share of generation increases when grids face stress, as seen in the U.S. and many parts of Asia and Europe.

Figure 4: A Three-Tiered Energy System

.png)

Sources: Adapted from Lars Schernikau, “Electricity for Data Centers . . . Is AI the Driving Force?,” The Unpopular Truth (blog), January 24, 2025. Data from Schernikau’s independent research and analysis.

* International Energy Agency (IEA), World Energy Outlook 2024 (IEA, 2024), 43.

Coal-fueled thermal power plants play a critical role in the physical stability of electrical grids.13 For fundamental physical reasons, large rotating synchronous machines (found in coal, gas, hydro, biomass, and nuclear power plants) are needed to ensure grid firmness and frequency stability. By contrast, wind and solar are not just intermittent—they deliver power through inverters, producing what is termed digital power. Digital power means that they are inherently based on power electronics that provide none of the vital grid characteristics that rotating, heavy-mass, synchronous machines with inertia provide.14 Utility-scale batteries also provide digital power. When sudden supply or demand disruptions occur, thermal plants with inertia are vital for keeping the grid stable and preventing cascading failures. The central trigger of the massive April 2025 Iberian Peninsula blackout—which affected some 50 million people—was the absence of that inertia on a grid that had been over-reliant on digital power, primarily solar.15

In addition to grid reliability and stability, coal offers strong energy security and affordability. Coal is cheaper than nuclear and gas (especially LNG) in most of the world, and months’ worth can easily and inexpensively be stored near power stations to meet sudden increases in demand. Countries with substantial domestic reserves—such as China, Colombia, India, Indonesia, Russia, South Africa, and the U.S.—benefit from regional sourcing and stockpiling to deliver reliable electricity at competitive cost, especially compared with European countries that significantly rely on imported LNG or weather-dependent renewables. Germany’s 2026 discussions on reactivating reserve coal capacity to manage costs amid LNG price spikes underscore coal’s critical role in diversified energy systems.16

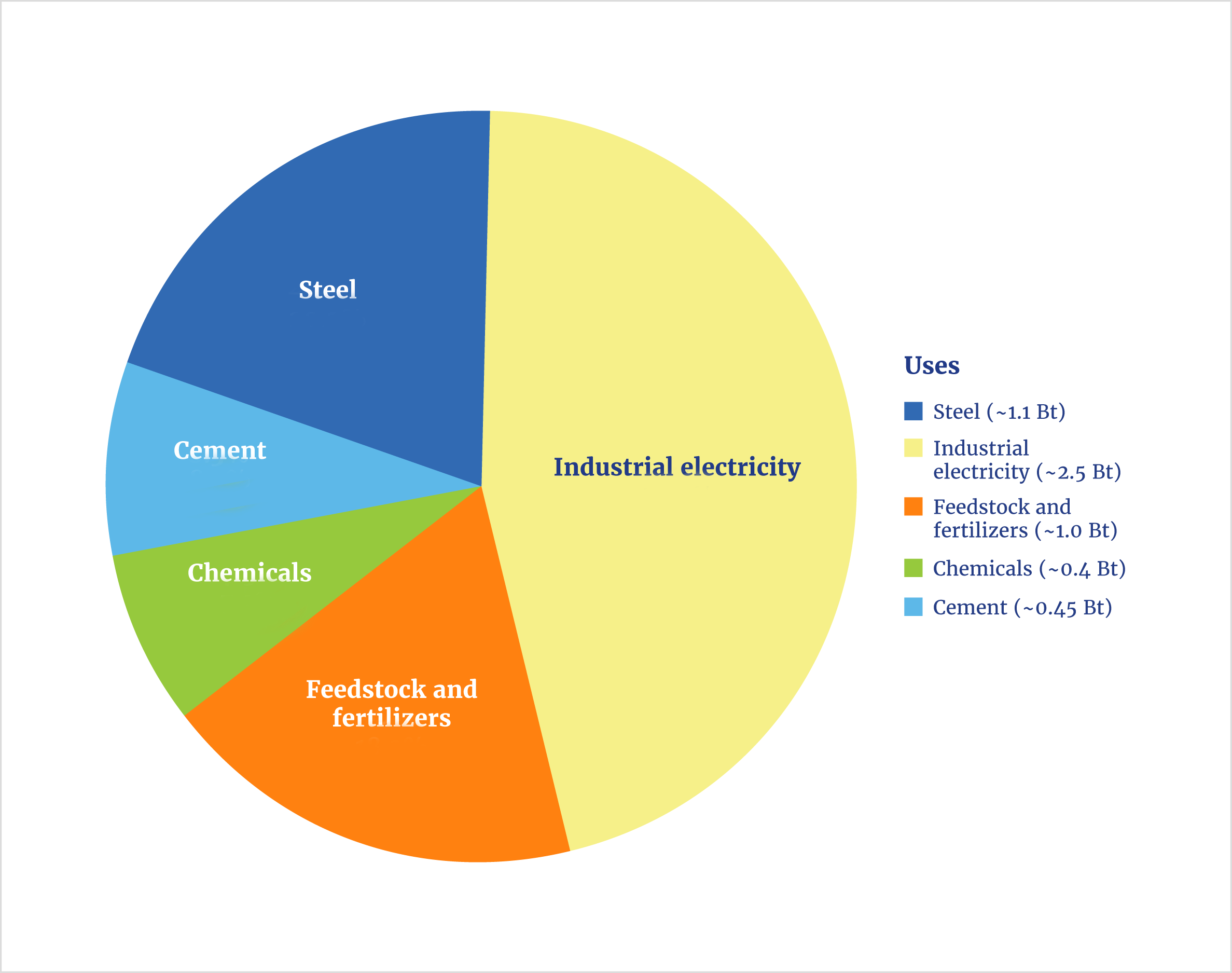

Then there are the industrial uses for coal that remain stubbornly irreplaceable. Of the estimated 9 Bt of coal consumed in 2025, well over half directly or indirectly supports industrial activity: steel, cement, chemicals, metals, manufacturing, and electricity for industrial processes such as smelting (see figure 5). Many industrial applications require sustained high temperatures (about 1,100–2,200 degrees Fahrenheit, or 600–1,200 degrees Celsius) and continuous operation, rendering intermittent solar and wind unsuitable and natural gas noncompetitive in most regions. (Some advanced nuclear designs promise suitable temperatures but remain largely aspirational.) Modern metallurgy depends on coal-derived carbon as a reductant to convert metal oxides into metals. Metallurgical coal produces coke for blast furnaces to turn iron ore into steel; refines other critical minerals; and reduces high-purity silica sand to silicon for solar panels, semiconductors, and computer hardware. Metallurgical coal accounts for about a quarter of seaborne coal trade.17

Global coal use continues to grow alongside increased demand for infrastructure, steel, and electricity, even as Europe shuttered 13 GW18 of coal generation in 2025—including the modern Moorburg power station in Hamburg, an approximately 1.6-GW plant that cost 3 billion euros to build and operated for only five years before its early closure and demolition.19 Meanwhile, coal-to-liquids production—a geopolitical hedge against diesel fuel and gasoline imports—is rising across Asia.20

Figure 5: Global Industrial Uses of Coal

Note: Total global industrial uses of coal are approximately 5.5 Bt per year. Bt denotes billion metric tons.

Source: Data from Schernikau’s independent research and analysis.

Fertilizer, Food Security, and Poverty Reduction

The nitrogen in fertilizers comes principally from the Earth’s atmosphere, which comprises 78% nitrogen (N₂). Plants cannot use N₂ directly. The Haber–Bosch process converts atmospheric nitrogen and hydrogen into ammonia (NH3), the foundation of nitrogen fertilizers.21

Coal supplies roughly 20% of global hydrogen for ammonia production and an even larger share of the feedstock for nitrogen fertilizers (urea, ammonium nitrate, ammonium sulfate), on which about 50% of the world’s population depends for food. Coal-based ammonia represents about a quarter of global output. In China, over 75% of hydrogen—the feedstock for ammonia—is coal-derived, which consumes about 100 Mt of coal annually. Globally, natural gas is used to produce about 70% of hydrogen feedstock, coal about 20%, and oil about 10%.22

A Major Trade and Supply-Chain Reality

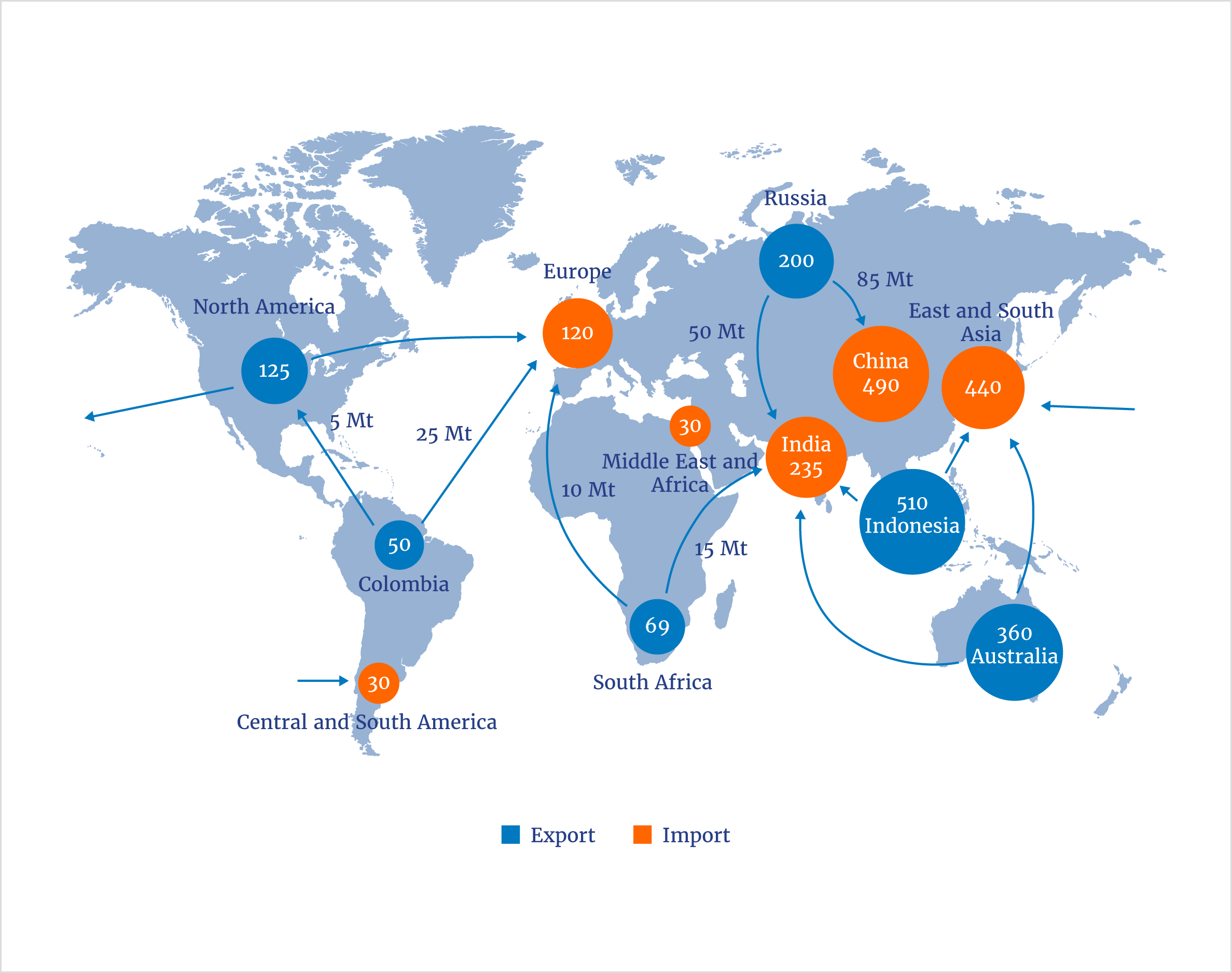

Markets provide a clear lens into the criticality of a commodity. Zooming out from coal’s roles in electricity, industry, and food production, global seaborne activity underscores its importance across regions (see figure 6). Of the more than 12 Bt of goods transported by sea annually, 5.5 Bt are energy commodities; coal alone accounts for 1.5 Bt of that total.23 On average, about 70% of seaborne coal trade is thermal coal for power plants.24

Figure 6: Global Coal Exports and Imports

Note: This figure shows approximate coal movement in 2025, totaling approximately 1.5 Bt. Bt denotes billion metric tons, and Mt denotes million metric tons. East and South Asia includes Japan, South Korea, Brunei Darussalam, Cambodia, Indonesia, Lao People’s Democratic Republic, Malaysia, Myanmar, the Philippines, Singapore, Thailand, and Vietnam.

Sources: Adapted from Lars Schernikau, “Coal Keeps the Lights On . . . Are We Experiencing a ‘New’ Renaissance of Coal?,” The Unpopular Truth (blog), March 18, 2026. Data from International Energy Agency (IEA), “Demand,” in Coal 2025—Analysis and Forecast to 2030 (IEA, 2025), 12–42; and additional calculations from Schernikau’s research and analysis, including HMS Bergbau AG demand and supply estimates.

Indonesia remains the leading seaborne coal exporter, shipping about 500 Mt annually, followed by Australia at about 360 Mt, and Russia at 200 Mt. The U.S., South Africa, and Colombia trail as smaller players in the seaborne market. Mongolia has emerged as the dominant overland exporter; it delivers about 90 Mt annually, mostly to China. The country may soon become the second-largest exporter of metallurgical coal in the world.25

Supply reliability is generally strong. Occasional disruptions arise from government policy (for example, temporary export bans in Indonesia) or weather-related issues in Australia and South Africa (floods and cyclones). These cause short-term dents in the supply chain but rarely threaten global supply meaningfully. The most recent significant disruption occurred when Western sanctions on Russian coal following the Ukraine invasion forced a major reshuffling of trade flows. Under normal market conditions, thermal coal prices tend to track power generation economics and are heavily influenced by competing fuel prices, particularly natural gas.

In 2025, China led seaborne coal imports with roughly 550 Mt, followed by India at about 240 Mt. ASEAN countries imported about 180 Mt, Japan about 140 Mt, and South Korea about 100 Mt. The EU imported roughly 120 Mt.26

Global supply-demand balances result from complex interactions between domestic production and consumption on the one hand, and trade on the other. In major players such as China, India, Indonesia, the U.S., and South Africa, internal shifts heavily influence prices and volumes available for seaborne trade. Domestic consumption outpacing production turned China from a net coal exporter into the world’s leading importer beginning in 2009.

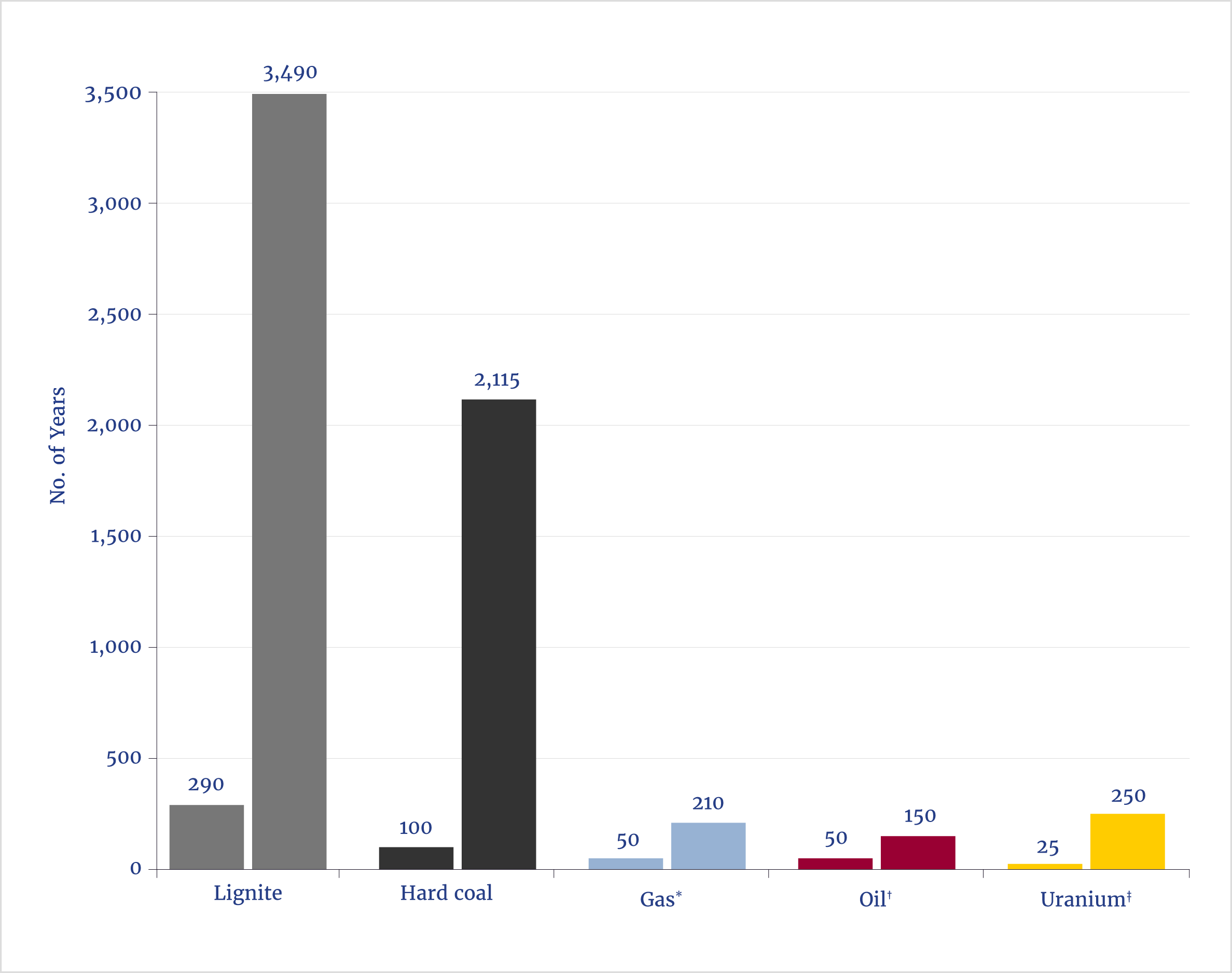

Thousands of Years in Reserves

Coal stands out for its geological abundance relative to current production rates. Total remaining coal reserves are estimated to last some 2,000 years for hard coal (anthracite and bituminous) and more than 3,000 years for lignite at today’s consumption levels.27Even counting only proven reserves (quantities economically recoverable with today’s technologies), global coal supplies should last 130–150 years.

By comparison, proven reserves of oil provide about 50–60 years of consumption; natural gas, about 50–55 years; and uranium, 50–100 years in known deposits for conventional reactors—with advanced technologies extending this significantly (see figure 7).28

Most importantly, coal deposits are widely distributed across many countries and continents. This geographical dispersion insulates the fuel from shipping chokepoints, pipeline dependencies, and geopolitical risks.

Figure 7: Reserves of Fossil Fuels—Primarily Coal—Are Enormous

Note: This figure uses 2023 data. Remaining potential equals reserves plus resources, and oil and gas include both conventional and unconventional reserves and resources. The left bars show the reserve/production ratio, and the right bars show the remaining potential/production ratio.

* Shows conventional and unconventional gas total.

† Shows conventional and unconventional oil total.

‡ Remaining potential includes only economically recoverable resources (<$80/kg).

Sources: Adapted from Lars Schernikau, “Coal Keeps the Lights On . . . Are We Experiencing a ‘New’ Renaissance of Coal?,” The Unpopular Truth (blog), March 18, 2026. Data from Bundesanstalt für Geowissenschaften und Rohstoffe (BGR), Energy Data 2024: German and Global Energy Supplies (BGR, 2025), consulted in the original German; and Schernikau’s independent research and analysis.

Technology and Pollution

Twenty years ago in Beijing, gray skies were common and face masks were part of everyday life. Today, official statistics indicate that Beijing could be considered pollution-free on about 95% of days in 2025.29

Following the launch of its war on pollution in 2013, China reported nearly 50% reductions in key urban air pollutants (including fine particulate matter pollution [PM2.5] declines of 50%–55% in Beijing and major cities by the mid-2020s) even as total coal consumption climbed to record levels. By replacing old coal plants with modern ones, installing advanced flue-gas controls, and relocating heavy industry away from population centers, China improved environmental outcomes while combusting ever more coal.

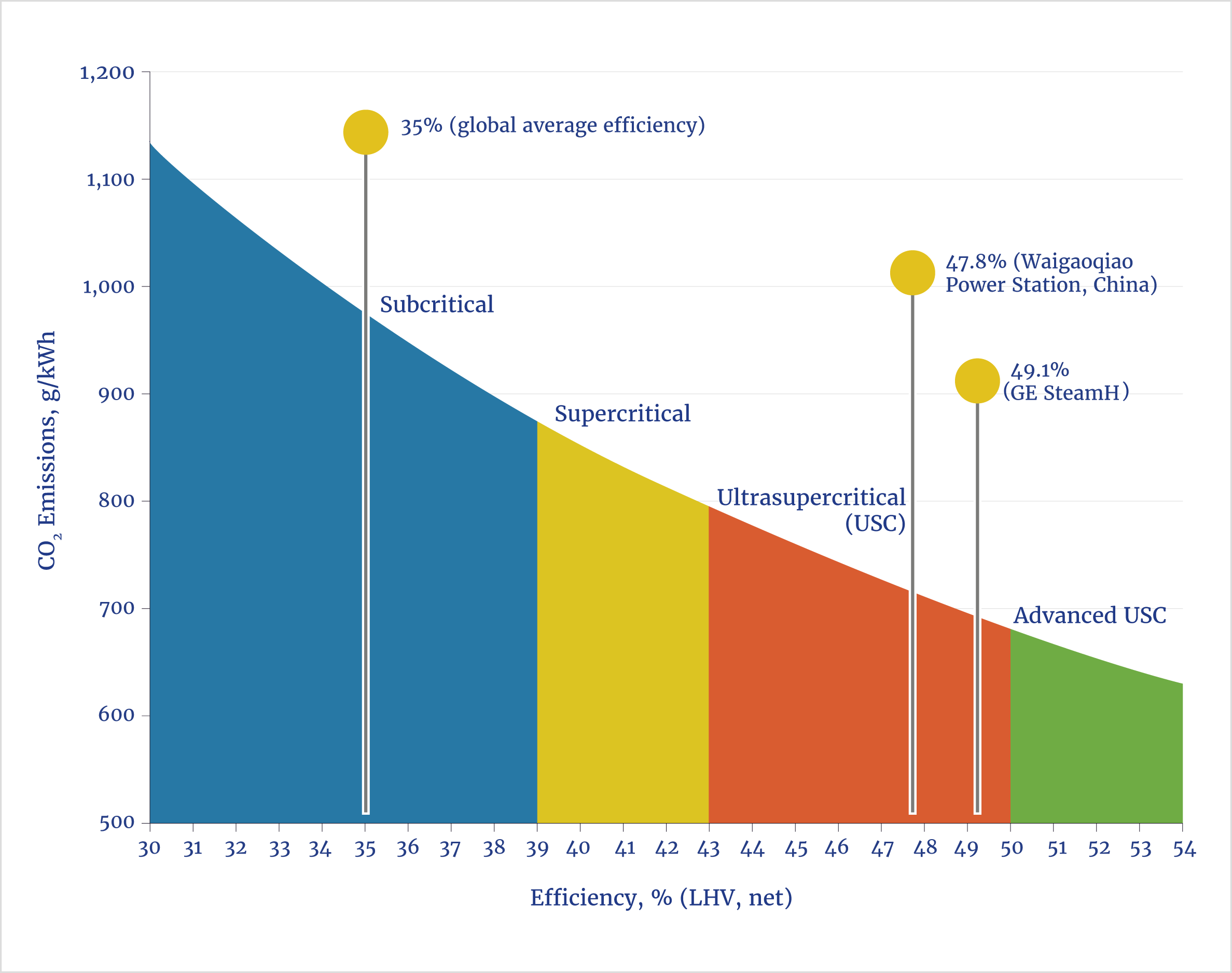

Modern coal-fired plants differ markedly from their predecessors (see figure 8). Compared with uncontrolled or twentieth-century technology, today’s state-of-the-art plants achieve emissions reductions of 99% for particulate matter,30 95%–99% for sulfur oxides, and 80%–90% for nitrogen oxides31 through electrostatic precipitators, flue-gas desulfurization, and selective catalytic reduction. In fact, through tall stacks and effective dispersion, a well-controlled modern coal plant can produce lower near-field ground-level particulate concentrations than a busy urban intersection.

Figure 8: Lowest-Cost Efficiency Pathway for Coal-Fired Power Plants

Source: Adapted from Lesley Sloss, Technology Readiness of Advanced Coal-Based Power Generation Systems, CCC/292 (IEA Clean Coal Centre, 2019), 18, figure 3.

All combustion technologies emit CO2, a gas with no direct toxicological harm to humans at ambient levels, which serves as essential plant food, acting as a powerful natural fertilizer by enhancing photosynthesis and water-use efficiency.32 Unlike traditional criteria pollutants, CO2 is fundamentally beneficial to plant life. Its primary environmental concern stems from its role in the atmospheric greenhouse effect. Global civilization measurably increases greenhouse gas concentrations. The magnitude and net consequences of future warming, climate sensitivity, and optimal policy responses remain subjects of active scientific and economic debate.33

Regardless of one’s views on long-term climate goals or the willingness of markets to pay for carbon capture and storage, real-world energy trade-offs persist.34

Arguments for disproportionately penalizing coal’s CO2 emissions relative to natural gas or other energy sources must account for the full life cycle, natural carbon uptake, system-wide emissions, reliability considerations, and non-CO2 greenhouse gases such as methane.35

Waste Streams

Global coal combustion produces roughly 1 Bt of coal ash and related residues annually. This is a large but relatively inert mineral waste stream (primarily silicon, aluminum, iron oxides) that is often reused in cement, concrete, and construction. By comparison, mineral extraction and processing required for wind, solar, and battery technologies generate smaller volumes of waste per unit of energy over time but can involve more chemically complex and potentially much more toxic tailings (see table 1). Many of these supply chains also rely heavily on coal-powered manufacturing.36

Table 1: Relative Toxicity of Waste Streams

.png)

* Bt denotes billion metric tons.

† Wind, solar, and battery waste was estimated for the year 2050.

Sources: Adapted from Lars Schernikau, “Coal Keeps the Lights On . . . Are We Experiencing a ‘New’ Renaissance of Coal?,” The Unpopular Truth (blog), March 18, 2026. Data from Schernikau’s estimates.

High-efficiency, low-emissions (HELE) technologies such as advanced ultrasupercritical plants improve thermal efficiency by reducing fuel consumption and emissions per kWh (see figure 8). China’s fleet upgrades demonstrate how retrofits and new plant construction can improve local air quality while expanding reliable baseload capacity. If older, low-efficiency plants worldwide were replaced overnight with state-of-the-art HELE units, global coal consumption could fall by nearly one-third while cutting criteria pollutants emissions by well over 90%.37

Perspective

Europe illustrates the risks of energy policies that prioritize environmental goals over energy security and affordability. With the notable exception of Poland, most EU countries have significantly displaced the use of domestic coal (and, in some cases, nuclear) in favor of imported natural gas and have increased the use of intermittent solar and wind. Following Russia’s invasion of Ukraine in 2022, several nations temporarily reactivated or extended the operation of lignite and coal plants to safeguard grid stability amid Russian gas-supply disruptions.38 Although U.S. LNG has become the dominant source—now accounting for nearly two-thirds of the EU’s LNG imports and growing39—European energy systems remain vulnerable to global gas market volatility and geopolitical unrest. Russia still supplied about 14% of the EU’s total natural gas in 2025, though this share continues to decline under phaseout measures.40 Germany, for example, decommissioned its highly efficient Moorburg coal plant (one of Europe’s most advanced coal facilities when built) as part of its coal phaseout,41 yet has periodically considered extending coal use during energy crises for cost and security reasons using older, less efficient coal plants.42 Many EU nations are coming to recognize the practical trade-offs of high reliance on intermittent wind and solar technologies.43

In the U.S., the Trump administration has moved to support domestic coal production through regulatory relief, federal land access, and technological development.44 This push is driven by surging electricity demand from data centers, AI infrastructure, and industrial reshoring, alongside a revived interest in energy security, reliability, and affordability. In 2025–26, the U.S. saw announcements and advancements of new coal projects and extensions; coal expansion is likewise underway in Australia, China (on a massive scale), India, Kazakhstan, Mongolia, Montenegro, and other countries. Nuclear and gas alone cannot meet the surging power demands of AI infrastructure. Terra Energy Center, which is developing a proposed coal plant in Alaska, is unlikely to remain the only North American data-center company turning to coal-fired power.45

Effective energy policy must balance real-world trade-offs across security, affordability, reliability, and environmental performance. While coal’s environmental impacts are real—as with all industrial-scale energy systems—the focus should be on technological improvements (clean coal via HELE and emissions controls) rather than premature elimination.

Coal remains foundational to modern civilization: Steel, cement, concrete, and most metals depend on it directly or indirectly in their supply chains. Without affordable, reliable baseload sources such as coal, energy costs rise, industrial capacity can become constrained, and broader economic outcomes may suffer46—especially today, with Western nations having offshored so much heavy industry to coal-reliant Asia.

This issue brief expands upon original research by coauthor Lars Schernikau published in “Coal Keeps the Lights On . . . Are We Experiencing a ‘New’ Renaissance of Coal?,” The Unpopular Truth (blog), March 18, 2026.

- Clyde Russell, “Iran War Gives Small Boost to Thermal Coal, Further Gains Possible,” Reuters Open Interest, May 5, 2026; Evan Millard, “Bangladesh Coal-Fired Generation Up on Year,” Argus Media, June 1, 2003; Agence France-Presse, “Philippines Declares ‘National Energy Emergency’ and Boosts Coal Power as Iran War Grinds On,” The Guardian, March 25, 2026; and “Viet Nam: Coal,” Countries & Regions: Asia Pacific, International Energy Agency (IEA), accessed June 22, 2026, https://www.iea.org/countries/viet-nam/coal.

- Eamon Farhat, “Europe Boosts Coal-Fired Power as Gas Prices Rally on Iran War,” Bloomberg, March 19, 2026.

- IEA, “Demand,” in Coal 2025—Analysis and Forecast to 2030 (IEA, 2025), 12–42.

- ASEAN Centre for Energy et al., Assessment of the Role of Coal in the ASEAN Energy Transition and Coal Phase-Out (ASEAN Centre for Energy, 2024), ix, xi.

- IEA, World Energy Outlook 2025 (IEA, 2025), 427, table A.2c.

- IEA, Financing the Modernisation of Power Systems Beyond Coal (IEA, 2026), 8, 27–31.

- Lars Schernikau, Economics of the International Coal Trade: The Renaissance of Steam Coal (Springer, 2010); Energy Institute, 2025 Statistical Review of World Energy, 74th ed. (Energy Institute, 2025), 52; and IEA, “Demand,” 13.

- IEA, “Demand.”

- Rongbin Xu et al., “Global, Regional, and National Mortality Burden Attributable to Air Pollution from Landscape Fires: A Health Impact Assessment Study,” The Lancet 404, no. 10470 (2024): 2447–59; and “Beijing Records Blue Skies on 95.3% of Days in 2025,” Livable Green Beijing News, The People's Government of Beijing Municipality, published January 5, 2026, https://english.beijing.gov.cn/specials/livablegreenbeijing/livablegreennews/202601/t20260105_4400731.html.

- Molly Lempriere, “New Coal Plants Hit 10-Year Global High in 2025, but Power Output Still Fell,” Carbon Brief, May 21, 2026.

- Biqing Yang, From Baseload to Flexibility: How Coal’s Role in China Is Changing (Ember, 2026); and Brian Hart et al., How Robust Is China’s Energy Security? (ChinaPower, 2025).

- Reuters, “India Will Use More Coal over the Next 25 Years, Report Says,” Reuters, February 10, 2026; National Institution for Transforming India (NITI) Aayog, Scenarios Towards Viksit Bharat and Net Zero: An Overview, vol. 1 (NITI Aayog, 2026).

- Dick Storm, “The Importance of Coal: Thermal Performance Considerations for Heat Rate and Resiliency,” Dick Storm’s Thoughts on Energy, Education, Economic Prosperity & Environmental Blog, February 8, 2026.

- Jonathan Lesser and Portia Roberts, Some Needed Realism on Wind Power (National Center for Energy Analytics [NCEA], 2026).

- Jared Leader et al., “What We Know—and Don’t—About the April 2025 Iberian Peninsula Power Blackout,” Smart Electric Power Alliance, May 9, 2025.

- Tom Schmidtgen and Joana Lehner, “Germany Considers Ramping Up Coal Power to Avert Energy Crisis,” Politico, March 27, 2026; and Martin Lynch, “Germany and Italy May Turn Back to Coal,” Industrial Info Resources, April 6, 2026.

- IEA, “Demand.”

- Lars Schernikau, “Coal Keeps the Lights On . . . Are We Experiencing a ‘New’ Renaissance of Coal?,” The Unpopular Truth (blog), March 18, 2026; Global Energy Monitor et al., Boom and Bust Coal 2025: Tracking the Global Coal Plant Pipeline (Global Energy Monitor, 2025); “Ratcliffe-on-Soar Power Station,” Power Plants in the U.K., Uniper, accessed June 25, 2026, https://www.uniper.energy/united-kingdom/power-plants-united-kingdom/ratcliffe-soar; and Schernikau’s independent research and analysis.

- “Hamburg-Moorburg Power Station,” Global Energy Monitor wiki, last modified June 26, 2026, https://www.gem.wiki/Hamburg-Moorburg_power_station.

- Grand View Research Conventional Energy Research Team, Coal to Liquid Market, 2024–2030 (Grand View Research, 2024).

- IEA, Ammonia Technology Roadmap (IEA, 2021).

- IEA, Ammonia Technology Roadmap.

- United Nations Conference on Trade and Development (UNCTAD), “International Maritime Trade,” in Review of Maritime Transport 2025: Staying the Course in Turbulent Waters (United Nations, 2025), 1–32.

- IEA, “Demand.”

- IEA, “Demand”; and additional calculations from Schernikau’s research and analysis, including HMS Bergbau AG demand and supply estimates

- IEA, Coal 2025—Analysis and Forecast to 2030 (IEA, 2025), 62.

- Bundesanstalt für Geowissenschaften und Rohstoffe (BGR), Energy Data 2024: German and Global Energy Supplies (BGR, 2025). This was consulted in the original German.

- BGR statistics likely underestimate uranium reserves.

- “Beijing Records Blue Skies.”

- A. L. Moretti and C. S. Jones, Advanced Emissions Control Technologies for Coal-Fired Power Plants, Technical Paper BR-1886 (Babcock & Wilcox, 2012), 4–5.

- Masaki Takahashi, Technologies for Reducing Emissions in Coal-Fired Power Plants, Energy Issues no. 14 (World Bank, 1998). Table 2 indicates that flue-gas desulfurization (FGD) reduces sulfur-oxides emissions by 80%–99%. Schernikau estimates that modern FGD achieves 90%–99%+ reductions, while wet FGD processes routinely achieve 95%–98%+ reductions.

- Karl B. Hille, “Carbon Dioxide Fertilization Greening Earth, Study Finds,” NASA, April 26, 2016.

- Steven E. Koonin, Unsettled: What Climate Science Tells Us, What It Doesn’t, and Why It Matters, updated and expanded ed. (BenBella, 2024); and Roger A. Pielke Jr. and Justin Ritchie, “How Climate Scenarios Lost Touch with Reality,” Issues in Science and Technology 37, no. 4 (Summer 2021):75–83.

- Jonathan Lesser, A Cost-Benefit Analysis of Using Direct Air Capture to Remove Atmospheric Carbon (NCEA, 2026).

- Lars Schernikau and William Smith, “ ‘Climate Impacts’ of Fossil Fuels in Today’s Energy Systems,” Journal of the Southern African Institute of Mining and Metallurgy 122, no. 3 (March 2022): 133–46.

- Lars Schernikau, “Coal’s Importance for Solar Manufacturing,” The Unpopular Truth (blog), May 9, 2024.

- “High Efficiency Low Emissions (HELE),” FutureCoal, accessed June 22, 2026, https://www.futurecoal.org/sustainable-coal/high-efficiency-low-emissions-hele; IEA, Technology Roadmap: High-Efficiency, Low-Emissions Coal-Fired Power Generation (IEA, 2012); and Ian Barnes, Upgrading the Efficiency of the World’s Coal Fleet to Reduce CO₂ Emissions (IEA Clean Coal Centre, 2014).

- Sam Meredith, “Ukraine War: Europe Turns to Coal as Russia Squeezes Gas Supplies,” CNBC, June 21, 2022.

- “EU Imports of Energy Products—Latest Developments,” Statistics Explained, Eurostat, European Union, accessed on June 25, 2026, https://ec.europa.eu/eurostat/statistics-explained/index.php?title=EU_imports_of_energy_products_-_latest_developments; and “Gas Consumption and Demand Outlook,” European LNG Tracker, Institute for Energy Economics and Financial Analysis (IEEFA), accessed July 25, 2026, https://ieefa.org/european-lng-tracker#section7. IEEFA estimates that the U.S. could provide 75%–80% of European LNG imports by 2030.

- “REPowerEU: Phase Out Russian Energy Imports,” European Commission, accessed June 26, 2026, https://energy.ec.europa.eu/strategy/repowereu-phase-out-russian-energy-imports_en.

- FCW Team, “Hamburg Advances Towards Becoming a Hydrogen Hub with Strategic Demolition of Moorburg Plant,” Fuel Cells Works, November 14, 2024.

- Schmidtgen and Lehner, “Germany Considers Ramping Up.”

- Megan Gildea and Clio Ho, “Europe’s Surging LNG Imports in 2025 Reshape Gas Supply Dynamics,” S&P Global, January 5, 2026.

- Exec. Order No. 14261, 90 Fed. Reg. 15517 (April 14, 2025).

- “Project Selections for Broad Agency Announcement DE-FOA-0003605, Restoring Reliability: Coal Recommissioning and Modernization (Topic 1),” U.S. Department of Energy, accessed June 26, 2026, https://www.energy.gov/hgeo/project-selections-broad-agency-announcement-de-foa-0003605-restoring-reliability-coal-0.

- Conall Heussaff, Decarbonising Competitiveness: Four Ways to Reduce European Energy Prices (Bruegel, 2024).

-6%20(9).png)

-3%20(1).png)